Europe’s ESG Reporting Faces Credibility and Compliance Challenges

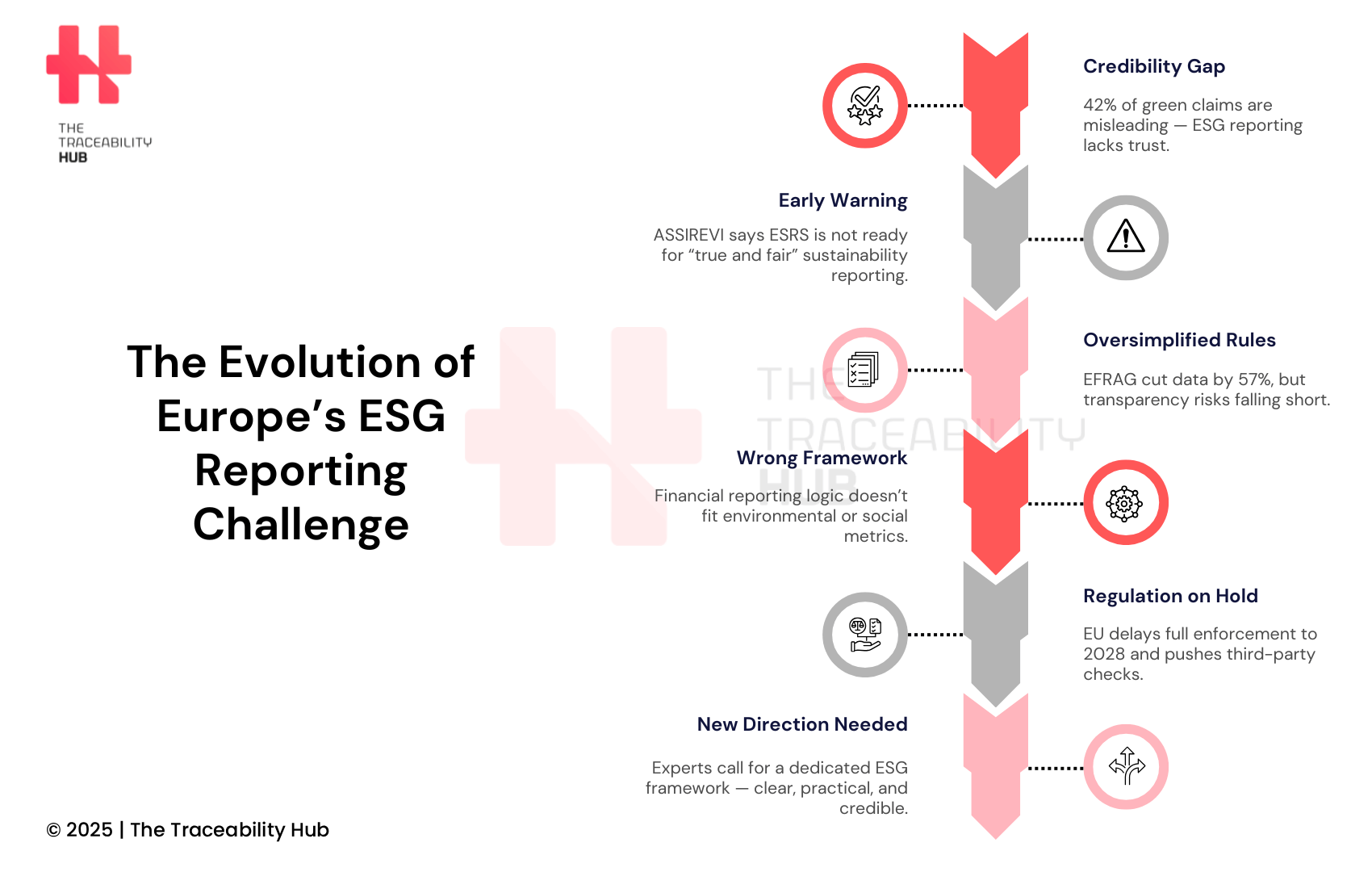

Companies face a credibility crisis in sustainability reporting. A 2021 European Commission study revealed that 42% of environmental claims were exaggerated, false or misleading. On top of that, it was found that all but one of these declarations lacked enough evidence to back their claims. Regulatory pressure for transparency keeps growing, yet industry experts warn that current reporting frameworks need more work.

The Italian association of audit firms, ASSIREVI, has raised most important concerns about the European Sustainability Reporting Standards (ESRS). “Suggesting that the ESRS standards system can lead to a true and fair representation regarding sustainability is premature,” ASSIREVI points out. The European Financial Reporting Advisory Group’s (EFRAG) efforts to make these standards simpler “are not yet sufficient”. This creates uncertainty for companies that must comply with the Corporate Sustainability Reporting Directive (CSRD).

Industry experts point to deeper problems in ESG reporting’s current approach. ASSIREVI warns that “Defining what is true and fair for everyone in advance is impractical. This risks litigation, uncertainties, and an effect opposite to simplification”. These issues surface as regulators try to create final sustainability reporting requirements that balance detailed disclosure with practical implementation.

ASSIREVI Warns ESRS Lacks Readiness for ‘True and Fair’ Reporting

European standard setters from France, Germany, and Spain have teamed up with ASSIREVI to propose major simplifications to the European Sustainability Reporting Standards (ESRS). The Italian association emphasizes a crucial concern: ESRS framework lacks maturity to provide “true and fair view” sustainability reporting. This concept, which comes from financial reporting, might not work well with ESG disclosure.

EFRAG made significant efforts to streamline the standards. They cut mandatory datapoints by 57% and reduced the overall length by more than 55%. These changes still don’t solve the core issues. ASSIREVI warns that applying financial reporting principles to sustainability metrics could create more problems than solutions.

The European Securities and Markets Authority (ESMA) worries that some simplifications might reduce transparency in companies’ climate transition efforts. Investor groups like Eurosif state that the 57% reduction in datapoints should be “an absolute maximum.” They believe further reductions would damage sustainable corporate reporting’s credibility.

EFRAG’s simplification process has drawn criticism because they conducted most sessions behind closed doors. This raises concerns about transparency in this vital revision. EFRAG activated six key simplification levers to balance reporting requirements with essential information. However, experts question if these changes address the unique challenges that separate sustainability reporting from traditional financial statements.

The Evolution of Europe’s ESG Reporting Challenge

Experts Highlight Risks of Applying Financial Logic to ESG Reporting

A philosophical debate goes beyond technical compliance issues about whether financial reporting concepts can work with sustainability measurement. Money falls short as a universal measure of environmental and social effects – this exposes a fundamental flaw when applying the “true and fair” financial model to ESG.

Critics point to what they call a “Nirvana fallacy” in current ESG thinking. This belief assumes perfect markets with fully informed players could price all externalities correctly. Prices actually show a complex mix of personal values, government policies, market conditions, and resource availability rather than objective truth.

Colin Mayer’s suggestion that companies should track “true costs” faces criticism as impractical. Critics argue that “it is not plausible to imagine that we can solve sustainability problems by effectively addressing market failures and achieving true pricing”.

Financial risk assessment has proven methods, yet a survey reveals 58% of financial institutions don’t manage ESG risk effectively. This gap demonstrates the core difference between classic financial risks and sustainability’s effects.

Competing values in ESG cannot be combined into a single, overarching measure. Shareholders who focus mainly on business concerns might not serve as the best guardians to prevent companies from causing social or environmental damage.

Regulators Urged to Refine ESRS Standards Before Enforcement

European regulators have started major changes to the ESRS framework due to growing concerns about its implementation. EFRAG started a 60-day consultation in July 2025 to simplify standards. The goal was to create “a more manageable and available reporting framework”. This change came after the European Commission asked to streamline requirements while protecting the main goals of the European Green Deal.

The suggested changes could cut the reporting requirements by more than half. Six keyways to simplify include an easier double materiality assessment and better report structure. Companies now have two extra years until 2028 to comply, thanks to a ‘stop-the-clock’ measure.

Third-party verification is a vital part despite these timeline changes. More stakeholders want external verification of ESG metrics. This becomes even more important as investors and regulators just need more confidence in sustainability data. Third-party assurance offers several benefits. These include data accuracy checks, finding reporting gaps, and increased stakeholder trust.

The biggest problems in ESRS implementation come from complex information management needs and new sustainability concepts. The ESG reporting scene keeps changing. Regulators and reporting entities face an ongoing challenge to balance strong standards with practical implementation. This is especially true when you have companies that the CSRD has brought into scope.

Why ESG Reporting Needs a Different Approach

Organizations face major challenges in sustainability reporting as they try to balance regulatory needs with real-world implementation. ASSIREVI’s warnings point to a key issue: sustainability metrics need their own framework rather than adopting financial reporting methods without proper evaluation. EFRAG has tried to simplify things by cutting datapoints by 57% and overall length by over 55%. These changes don’t solve the basic problems.

The push for standardization might create more issues than it solves. Financial reporting’s “true and fair” concept doesn’t work well with environmental and social measurements. We struggled to use money-based metrics as universal measures for sustainability factors. Companies now must meet compliance rules while dealing with practical issues in collecting, checking, and reporting ESG data.

European regulators understand these challenges and have revised the ESRS framework. They added a two-year compliance window until 2028 because businesses need time to adapt to these new standards. Third-party verification plays a vital role in building stakeholder trust despite these implementation hurdles.

Sustainability reporting needs its own unique approach, different from traditional financial disclosure. Companies should develop systems specifically for sustainability’s unique features instead of forcing ESG metrics into existing frameworks. This approach would help avoid wasting resources on compliance without achieving real transparency. Future corporate reporting success depends on finding the right balance between detailed disclosure and practical implementation.

Read more: The Biggest Pain Points of the Fashion and Sportswear Industry Today