CBAM in One Page: What Companies Need to Know

The Carbon Border Adjustment Mechanism (CBAM) is the EU’s instrument to put a fair carbon price on certain carbon-intensive goods imported into the EU. In practice, CBAM aligns the carbon cost of imports with the carbon cost EU producers face under the EU Emissions Trading System (EU ETS), helping prevent carbon leakage, the shift of carbon-intensive production and embedded emissions to countries with less stringent climate policies.

By linking trade, emissions, and carbon pricing, CBAM directly connects supply chain emissions data, import compliance, and financial exposure.

What CBAM Is (and Why It Exists)

CBAM exists to protect the integrity of EU climate policy. As the EU raises its climate ambition, there’s a real risk that emissions don’t disappear; they simply move. Carbon leakage happens when companies relocate production abroad or when EU products are replaced by more carbon-intensive imports.

CBAM is designed to counter that by ensuring that imports carry a carbon price equivalent to domestic EU production. This supports decarbonization while maintaining a level playing field for the EU industry.

Products Currently in Scope

CBAM does not apply to every imported product. Today, it targets a defined set of sectors that are both carbon-intensive sectors and exposed to leakage risk. Currently, CBAM scope includes six product categories:

- Cement

- Iron and steel

- Aluminium

- Fertilizers

- Electricity

- Hydrogen

For companies, the practical implication is simple: CBAM relevance is determined at the product level, and the first step is knowing whether your imported goods fall within CBAM scope.

Timeline that Matters for Companies

CBAM has been introduced gradually, with a deliberate transition from reporting obligations to financial exposure tied to embedded emissions.

CBAM began its transitional phase on 1 October 2023. During this period, the focus is on collecting and reporting embedded emissions data, a learning period for importers, suppliers, and authorities. No CBAM certificates are purchased in this phase.

This stage is essentially the system “warming up”: companies build internal processes; suppliers begin responding to emissions data requests, and authorities refine operational procedures.

The definitive CBAM regime starts on 1 January 2026. This is the point where CBAM moves from a reporting exercise to a fully operational and financial mechanism tied to embedded carbon emissions.

At a high level, the definitive system works like this:

- Importers declare the embedded emissions in CBAM goods and surrender CBAM certificates annually.

- The certificate price is linked to the EU ETS allowance price (€/tCO₂).

- If a carbon price has already been paid in the country of production—and the importer can prove effective payment—an equivalent amount can be deducted.

From 2026 onward, CBAM becomes something procurement, finance, sustainability, and customs teams must manage CBAM together, because the data affects the financial bill.

Why Data Quality Directly Impacts CBAM Costs

CBAM is not just about compliance. It directly affects the cost. The number, and therefore the total cost of CBAM certificates, depends on the embedded emissions you report.

And the key nuance is this: the EU framework can only reward accuracy when you can prove it. Adjustments are only possible when you have evidence of, for example, supplier emissions data, methodology alignment, and documented carbon prices paid abroad. That means poor data doesn’t just create headaches reporting; it can translate into financial loss.

Weak, missing, or inconsistent data increases two things at once:

- Cost exposure, because emissions may be overstated, and deductions may be impossible to claim.

- Compliance friction, because low-quality inputs create rework, delays, verification problems, and reporting errors.

This is why CBAM readiness is best understood as a data + systems + supplier readiness challenge, not a tax or customs formality. If you approach CBAM as a spreadsheet-driven compliance task, you’ll be trying to manage a financial obligation with fragile inputs, exactly where cost and risk compound.

That’s the baseline. Next comes the practical question: are your products, suppliers, emissions data, and systems CBAM-ready?

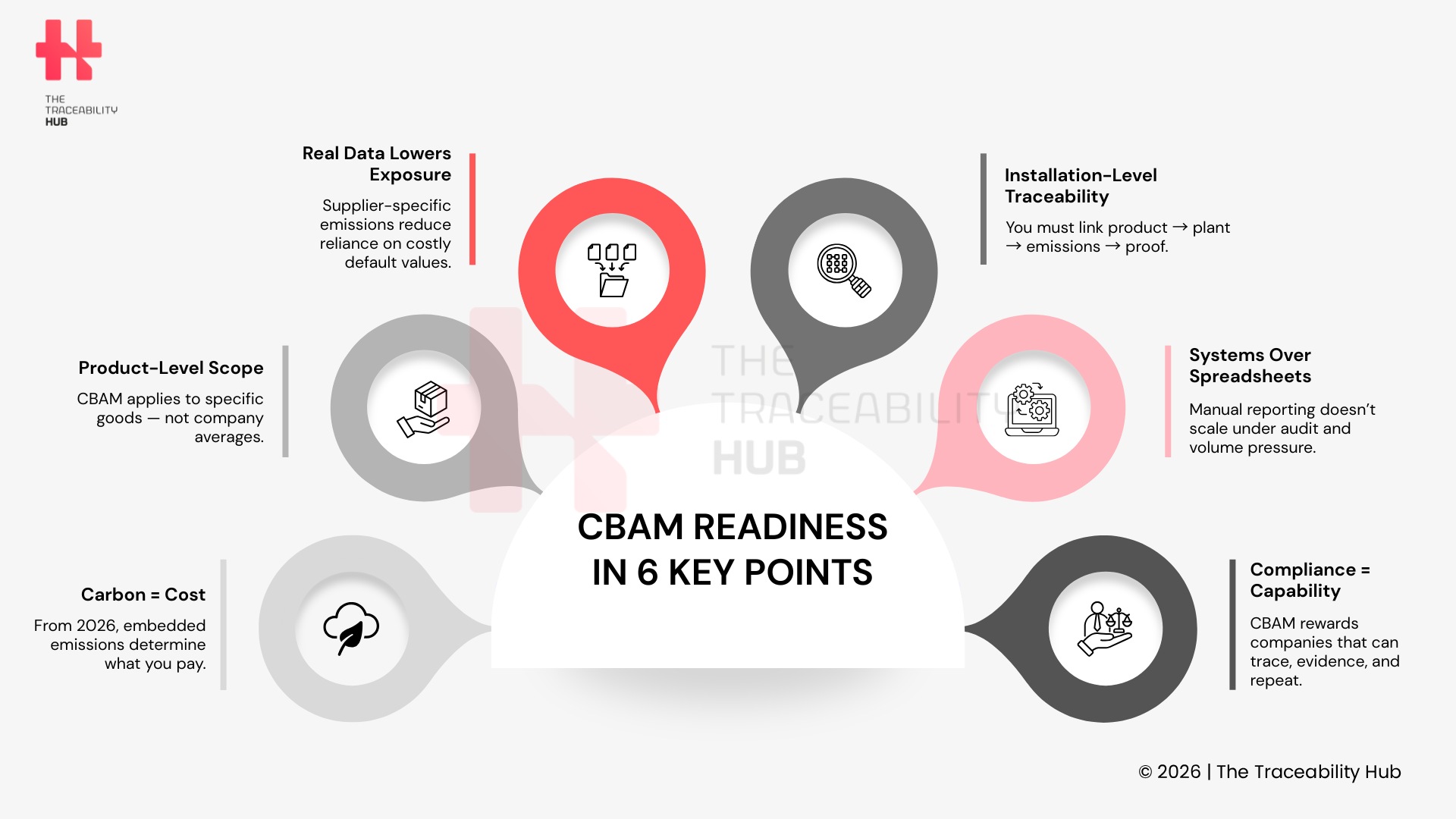

CBAM Readiness in 6 Key Points

CBAM Readiness Is a Data Problem First

One of the most common mistakes companies still make is treating CBAM as “tax compliance.” CBAM is the first and foremost data readiness and data governance challenge. Your ability (or inability) to collect, validate, and govern emissions information at installation level and product level will determine how manageable CBAM becomes, and how expensive it gets over time.

From 1 January 2026, imports of in-scope goods fall under the definitive CBAM regime and create financial exposure linked directly to embedded emissions. And even if certificate purchasing starts later, the cost of liability is triggered by the imports themselves. That shifts the conversation internally: it’s no longer enough to “submit a report.” You need a repeatable, audit-ready data backbone that can handle volume, complexity, and annual CBAM reporting cycles.

Why CBAM Depends on Installation-Level and Product-Level Emissions Data

CBAM is not built for corporate averages or generic ESG metrics. It relies on data that connects:

- the imported product (and its CN code)

- the production location and route (the installation/facility)

- the embedded emissions allocated to that product from that installation

This level of granularity is not a technical detail; it is the mechanism. Because the number of CBAM certificates (and therefore the cost) depends on the emissions you declare. If the data is incomplete, inconsistent, or not defensible, the risk is not just “bad reporting.” It becomes higher cost exposure, greater volatility, and more operational friction.

In simple terms: CBAM turns supply chain emissions data into a procurement cost driver.

Actual Supplier Data vs. Default Values: The Decision that Shapes Your Cost

In practice, under CBAM, companies have two routes to embedded emissions values under CBAM:

- Real, supplier-provided emissions data (actual values)

This is installation- and product-specific emissions data, calculated in line with CBAM methodologies, supported by evidence, and prepared for scrutiny. When you can obtain robust actual data, you can:- avoid overstatement,

- manage CBAM exposure proactively,

- forecast CBAM costs more realistically,

- compare suppliers on a like-for-like basis,

- and build a credible pathway for improvement with your supply base.

- Default values (fallback values)

When suppliers can’t provide complete, CBAM-aligned data, or can’t provide it on time, importers may have to rely on default values. This is where CBAM becomes financially painful: defaults are intentionally conservative and punitive, designed to encourage the use of verified, supplier-specific data.

Operationally, default values mean loss of cost control.

And commercially, it creates pressure: if missing data increases your cost, that cost will eventually show up in supplier negotiations, sourcing decisions, and preferred-supplier status.

Why Spreadsheets and Manual Declarations Don’t Scale

During the transitional phase, many companies managed CBAM with email threads and Excel files to manage CBAM reporting. That was understandable: it was a pilot period. But under the definitive regime, this approach breaks quickly, for three structural reasons:

- Too many data points, too many iterations: data volume and interaction

CBAM requires precise information (installation details, production routes, direct/indirect emissions where applicable, allocations, supporting documents, carbon price paid evidence, etc.). Across dozens of suppliers and multiple CN codes, the workload multiplies fast. - You can’t control data quality at audit level: audit-level data control

Spreadsheets don’t provide strong audit trails, version control, consistency checks, anomaly detection, or structured management of missing data. The risk isn’t only making mistakes – it’s being unable to demonstrate how numbers were derived. - CBAM is not a one-off project, it’s an operating capability

This repeats every year. Volumes fluctuate. Suppliers change. Data needs updates. Deadlines don’t move. If your process is manual, every cycle becomes a fire drill- and internal costs rise alongside compliance risk.

The key point: CBAM readiness is not just “can we produce a report?”. It’s “can we do this repeatably, defensibly, and at scale without disrupting procurement and operations?”

That’s the lens to bring into the checklist: not as a compliance certificate, but as a maturity test across data, suppliers, and systems.

The CBAM Readiness Checklist

Most CBAM guidance focuses on what the regulation says. This checklist focuses on what companies need to be ready: data, systems, and suppliers.

Use it as a diagnostic tool, not a compliance certificate. The goal is to surface gaps early, before they show up as higher costs, delayed submissions, supplier disruption, or last-minute fallback to punitive assumptions.

Checklist Area 1 — Scope & Product Mapping

Are all your imported goods correctly mapped against CBAM scope?

CBAM applicability is determined at the product/CN-code level. Misclassification creates immediate reporting risk and can also distort cost forecasts.

- Products in scope clearly identified

- CN codes validated (not assumed from product names or commercial descriptions)

- Import volumes tracked by CN code and supplier

- De minimis check applied correctly: the 50-tonne threshold excludes many low-volume importers, but it does not exempt electricity and hydrogen (which remain in scope regardless of volume)

Have you identified who the CBAM declarant is, and which suppliers and installations generate embedded emissions?

CBAM obligations sit with the EU importer (or indirect customs representative), but compliance depends on emissions data tied to where production happens (the installation), not just who sells the goods.

- CBAM role clarity (who is the declarant under your trade terms / Incoterms)

- Direct suppliers identified (Tier 1)

- Production installations/facilities mapped where available

- Relevant upstream production steps understood (especially for precursors and complex value chains)

Checklist Area 2 – Emissions Data Readiness

Can you distinguish direct emissions, and indirect emissions where applicable, for each product?

You need clarity on emissions categories to avoid inconsistent reporting and to prepare for verification-grade scrutiny.

- Process (direct) emissions captured and product-allocated

- Energy-related (indirect) emissions captured where applicable by sector/product rules (don’t assume the same requirement applies to every CBAM good)

- Allocation logic documented (how installation-level emissions are assigned to product output)

Are emissions calculated using EU CBAM methodologies (and documented accordingly)?

Having “some emissions data” isn’t enough if it’s calculated using incompatible methods (e.g., generic ESG averages, corporate-level intensity metrics, or non-aligned national rules).

- Alignment with CBAM calculation rules and system boundaries

- Clear documentation of assumptions, data sources, and allocation approach

- No reliance on incompatible standards that can’t be reconciled to CBAM requirements

Do you have access to upstream (Tier 2+) emissions data where required, and do you know your gaps?

Many CBAM goods (and especially goods with relevant precursors) require upstream data to avoid blind spots and inflated values.

- Multi-tier visibility in place (or a defined plan to build it)

- Known data gaps documented (what’s missing, from whom, and why)

- No “unknown blind spots” (areas where you don’t even know what you’re missing)

Checklist Area 3 – Supplier Engagement & Capability

Do non-EU suppliers understand CBAM, and what installation-level data must they provide?

If suppliers don’t understand CBAM, timelines slip and data quality degrade, pushing you toward default values and higher exposure.

- Supplier awareness confirmed (not assumed)

- Clear data ownership on the supplier side (who compiles, validates, and signs off)

- Suppliers understand consequences of missing/late/unsupported data (cost impact, escalation, commercial friction)

Can suppliers provide repeatable, year-on-year emissions data (not one-off estimates)?

CBAM is an operating cycle. A single spreadsheet exercise won’t hold up over multiple reporting years.

- CBAM data can be reproduced consistently each year

- Suppliers have internal measurement capability (or a credible support plan)

- Data format, definitions, and submission workflow are standardized

Checklist Area 4 – Verification & Trust

If you use actual (supplier-specific) emissions values, can they be verified by an accredited third party?

Actual values can reduce cost exposure, but only if the dataset is verification ready. This is where many “good” numbers fail in practice.

- Audit trail available (inputs, calculations, evidence)

- Documentation quality is verification-ready (boundaries, allocation, sources)

- Risk of rejection assessed (unclear assumptions, missing evidence, inconsistent values)

Do you have evidence for carbon prices already paid in third countries (where applicable)?

Deductions depend on proof. Without defensible evidence of effective payment, you may lose cost relief.

- Applicable carbon pricing instruments identified (taxes, ETS, levies)

- Proof of “effective payment” collected and stored

- Clear mapping between the paid carbon price and the emissions/cost elements it covers

Checklist Area 5 – Systems & Reporting Infrastructure

Do you have a scalable system to collect, store, update, and report CBAM data, and manage authorization workflows?

Manual handling breaks at scale, especially across multiple CN codes, suppliers, installations, and reporting cycles. Systems readiness is also tied to registry processes.

- Automated or semi-automated data collection (not email + scattered spreadsheets)

- Central storage with version control, permissions, and auditability

- Integration with procurement, sustainability, customs, and/or ERP systems

- Readiness to produce structured outputs for CBAM Registry reporting

- Operational readiness for authorized CBAM declarant workflows and deadlines (including handling imports while authorization is pending where permitted)

From Checklist to Action Plan

A checklist only creates value if it leads to decisions. Once you have assessed your CBAM readiness, the next step is to convert identified gaps into a structured action plan that reduces compliance risk and financial exposure for imports subject to CBAM from 1 January 2026.

CBAM is no longer a learning or transitional exercise. Under the definitive CBAM regime, importers are now responsible for submitting accurate declarations supported by defensible data and documentation. The quality of your preparation now directly affects operational friction, regulatory audit risk, and cost control.

Prioritize Where CBAM Exposure Is Highest

Start by focusing on the areas where errors, CBAM data gaps, or fallback approaches have the greatest financial and compliance impact.

Priority should be given to:

- High-volume imports, as CBAM obligations scale with the quantity of goods released for free circulation in the EU

- Goods currently within CBAM scope: cement, iron and steel, aluminum, fertilizers, hydrogen, and electricity

- Trade flows with weak supply chain traceability to production installations, where it is difficult to identify where and how goods were produced

- Imports are likely to rely on default emissions values, because supplier-specific, installation-level data is not available, incomplete, or non-CBAM-aligned

Outcome: a ranked list of products, CN codes, and trade flows that require immediate action to avoid elevated compliance and financial risk.

Segment Suppliers by CBAM Readiness

CBAM compliance depends on supplier data capability. Segment suppliers based on their ability to support CBAM-aligned data requirements, not just commercial importance.

Typical CBAM readiness segments include:

- Operationally ready

Suppliers can provide installation-linked emissions data, calculated under CBAM methodologies, with clear documentation and internal sign-off processes. - Partially ready

Suppliers with some data available, but with gaps in methodology alignment, allocation logic, documentation quality, or internal governance. - Not ready

Suppliers are unable to provide usable installation-level data, creating a high likelihood of fallback approaches and repeated CBAM remediation. - Strategic but constrained

Critical suppliers facing structural challenges such as multi-installation production, complex precursor chains, or limited verification capacity.

Outcome: a supplier engagement and escalation strategy that targets effort where it materially improves CBAM outcomes.

Decide Where to Invest and Where to Accept Conservative Fallback

For each product and supplier segment, companies must make explicit decisions about where to invest resources and where to accept conservative CBAM fallback assumptions.

Key decision areas include:

- Data collection

- Standardize CBAM data requests to ensure consistency across suppliers

- Ensure data is linked to production installations and supported by documentation

- Align internal data collection cycles with annual CBAM reporting needs, while maintaining interim monitoring for control and forecasting

- Supplier engagement

- Establish clear data ownership and accountability on the supplier side

- Define escalation paths for incomplete, late, or unusable emissions submissions

- Provide CBAM guidance and templates where supplier capability is limited

- Data defensibility and verification readiness

- Focus early effort on documentation quality, traceability, and internal controls

- Treat CBAM verification readiness as an ongoing process, not a one-off exercise

- Identify suppliers and data sets where defensibility is critical to managing CBAM cost exposure

- Systems and traceability infrastructure

- Move beyond ad hoc email and spreadsheet-based CBAM processes

- Centralize CBAM-relevant data with version control, access management, and audit trails

- Connect customs data (CN codes, volumes) with sustainability and procurement systems to ensure consistency across reporting and internal decision-making

Outcome: a focused investment plan that reduces CBAM risk exposure is material, without overengineering low-impact areas.

Establish CBAM as an Operating Rhythm

Under the definitive regime, CBAM must be managed as a recurring operational process rather than a one-time compliance project.

A practical CBAM operating rhythm typically includes:

- Ongoing monitoring: Tracking import volumes, supplier data status, and emerging data gaps throughout the year.

- Annual consolidation: Preparing a complete, defensible dataset for the annual CBAM declaration, supported by documentation suitable for regulatory scrutiny.

This approach reduces last-minute remediation, lowers audit and enforcement risk, and improves internal control over CBAM-related exposure.

Why CBAM Readiness Becomes a Traceability Advantage

CBAM is often described as a carbon “border charge.” But for most businesses, the real shift is more operational than political: CBAM makes product-level carbon transparency part of day-to-day trade. It doesn’t reward companies with the best sustainability narrative. It rewards the ones that can trace, evidence, and repeat.

From 1 January 2026, CBAM moved into its definitive phase. That matters because the burden is no longer just “report something.” It’s “report the right thing”, at the level of the imported good, linked to where it was produced, and supported by information that can stand up to scrutiny. In other words, CBAM turns carbon data into a regulated supply chain asset.

CBAM Accelerates Product-Level Carbon Transparency

For years, carbon data lived mostly in corporate reporting, high-level footprints, broad assumptions, and aggregated Scope 3 models. CBAM shifts the center of gravity toward embedded emissions tied to real production. The closer your data sits to the product and the installation, the more control you have over outcomes.

That’s why CBAM readiness isn’t just a compliance exercise. It’s a forcing function for traceability: mapping products to CN codes, linking flows to suppliers and production sites, and managing emissions inputs the way you manage financial data, structured, documented, and consistently.

Traceability Turns Supplier Engagement from Chaos into a Workflow

CBAM readiness changes supplier conversation. It’s no longer enough for a supplier to share a generic ESG report or a marketing claim. Importers need installation-specific emissions information that is repeatable, and usable within CBAM reporting logic.

Companies with traceability capabilities can make this easier by standardizing requests, creating clear data ownership, and tracking responses across a supplier base without endless email threads. The result isn’t just faster data collection. It’s less friction, clearer expectations, and better supplier relationships.

Better Traceability Means Lower CBAM Compliance Risk

When CBAM data is incomplete or inconsistent, the problem is rarely one missing number. It’s a missing chain of evidence: which site produced the goods, what methodology was applied, what boundaries were used, and whether the figures can be defended.

Traceability reduces that risk by design. It creates a single line of sight, from import flows to product identifiers, to the producing installation, to the emissions of data and supporting documentation. That audit-ready structure is what prevents last-minute firefighting, rework, and avoidable cost exposure.

CBAM Isn’t a One-Off: It’s a Template for What Comes Next

CBAM signals a broader direction: regulation that is enforced through granular, structured, auditable supply chain data. Once you build traceability for CBAM, you’re not just “ready for CBAM”. You’re building a repeatable operating capability for the next wave of product-level transparency and trade-linked sustainability rules.

CBAM readiness is a strategic advantage when it’s treated as traceability capability. Companies that invest early don’t just reduce compliance risk, they improve supplier collaboration, build stronger data foundations, and position themselves to compete in a world where “we can prove it” matters more than “we say it.”

Read more: Smart Packaging Technologies for Food Safety, Quality, and Sustainability