Bridging the Rural Digital Divide in European Agriculture

The digital divide in agriculture remains a structural challenge across Europe and continues to shape the pace of digital transformation in agriculture. While overall internet access has improved significantly, rural areas still lag behind urban regions, particularly in access to high-speed and very high-capacity broadband infrastructure. This connectivity gap directly affects the agricultural sector, where many traditional farms struggle to leverage real-time market data, precision agriculture technologies, and digital sales channels that could enhance efficiency, competitiveness and long-term economic resilience.

The issue is particularly relevant in countries such as Italy, where Italian agriculture is characterized by small-scale and family-run farms that often operate with limited digital infrastructure and constrained investment capacity. Bridging this digital divide into agriculture requires targeted and practical interventions. Cooperative technology models, public funding mechanisms, and mobile-first digital farming solutions tailored to rural connectivity constraints represent viable and scalable approaches to strengthening digital adoption in agriculture.

Understanding the Digital Divide in Italian Agriculture

What Is Digital Agriculture?

Digital agriculture refers to the use of digital technologies to collect, store, analyze, and share data across agricultural systems. The Food and Agriculture Organization of the United Nations (FAO) describes this transformation as part of a broader digital transformation in agriculture, where data-driven technologies are reshaping farming operations supply chains and agri-food markets. These innovations extend beyond traditional on-farm practices and increasingly influence the entire agri-food value chain – before, during and after production.

The scope of digital agriculture technologies includes precision farming techniques such as yield mapping, GPS-guided machinery, IoT and sensors, and variable-rate input applications. It also encompasses digital marketplaces, warehouse receipt systems, traceability solutions, farm management software, and equipment-sharing applications. Underpinning these digital farming systems are enabling technologies such as cloud computing, big data analytics, artificial intelligence (AI), machine learning, the Internet of Things (IoT), and digital communication networks.

Farmers today deploy sensors, drones, satellite imagery, and, in some contexts, robotics to optimize farming operations, improve resource efficiency, and support data-driven decision-making. These technologies can enhance productivity while reducing input waste and environmental impact. In more advanced contexts, robotics and automation complement these tools, strengthening the integration of precision agriculture within larger production systems.

Smartphones and connected devices have significantly expanded access to agricultural information and services. They enable near real-time monitoring, faster operational decisions, and improved coordination across supply chains. While digital adoption in agriculture levels vary by region and farm size, digital tools increasingly support more informed crop and livestock management practices.

The Meaning of the Digital Divide for Traditional Farms

The digital divide in agriculture refers to disparities in access to, and effective use of digital technologies within the farming sector. It extends beyond simple device ownership or internet connectivity. The divide encompasses the ability to integrate digital agriculture tools into farm management, improve productivity, access markets, strengthen traceability systems, and enhance overall livelihoods.

In high-income contexts, farms may deploy sensor networks, satellite imagery, and data analytics to optimize irrigation, fertilization, and crop protection strategies. In contrast, smallholder farmers in lower-income or infrastructure-constrained regions may lack reliable mobile connectivity to access basic services such as market prices, weather forecasts, apps, or digital payment systems. This uneven access reinforces the broader rural digital divide and limits equitable participation in digital transformation in agriculture.

The digital divide is driven by multiple, interconnected factors: socio-economic conditions, rural infrastructure gaps, affordability constraints, and varying levels of digital literacy. Unequal access to information and communication technologies (ICTs) can result in uneven digital adoption in agriculture and, consequently, unequal distribution of productivity and income gains. Digital transformation requires not only infrastructure but also technical capacity, advisory support, and enabling policy frameworks.

Smallholder farms represent approximately 84% of all farms globally, yet they operate only about 12% of the world’s agricultural land. Despite this relatively small land share, they are estimated to produce roughly one-third of global food supply (figures vary between 30–35% depending on methodology and region). Their contribution to food security is therefore significant within global agri-food systems. However, smallholders often face structural constraints including climate vulnerability, market volatility, limited access to finance, low productivity, and inefficient supply chains.

Without access to digital business management tools, precision agriculture technologies and scalable traceability systems, small-scale producers and cooperatives may struggle to compete in increasingly digitized agri-food markets. While insolvency is not inevitable, limited digital integration can reduce competitiveness and resilience over time.

Why Italy’s Small Farms Face Structural Challenges

Italian agriculture is characterized by a high prevalence of small and medium-sized farms, many of which specialize in high-quality, geographically distinctive productions such as extra virgin olive oil, wine and PDO/PGI-labelled products, with a certified and protected origin and territory. While these small farms in Italy contribute significantly to rural economies and product excellence, they face mounting structural pressures.

Recent agricultural census data confirm a clear process of structural consolidation in Italy’s farming sector. According to the 7th General Census of Agriculture (2020), Italy had approximately 1.06-1.13 million agricultural holdings in 2020, representing a decline of about 32 % compared with 2010. At the same time, the average utilized agricultural area (UAA) per farm increased, with the 2020 figure at roughly 10.7-11.1 hectares per holding, up from smaller averages in earlier decades. This pattern reflects ongoing structural contraction and concentration, as numerous smaller farms close or merge, and remaining operations manage larger areas of land.

For small-scale producers and traditional farms, including many olive oil growers, rising production and management costs present persistent challenges. These include higher processing and energy costs, labour shortages (particularly seasonal and skilled labour), and constrained access to credit. At the same time, climate-related risks have intensified. Extreme weather events such as heatwaves, droughts, hailstorms and late frosts increasingly affect yields, while plant diseases and pest infestations – including the well-documented spread of Xylella fastidiosa in olive groves – have severely affected olive production in certain regions.

Market access represents another structural bottleneck. Many small farms remain dependent on intermediaries and wholesale channels, limiting their ability to capture premium value for high-quality production. Price volatility and global competition further compress margins. While farm abandonment and land sales do occur, especially in marginal areas, the trend is better described as gradual structural adjustment rather than collapse.

Digital agriculture tools offer potential mitigation pathways. Direct-to-consumer e-commerce platforms, digital traceability systems that communicate product value, data-driven agronomic tools, and improved weather forecasting services can enhance resilience and competitiveness. Precision agriculture technologies may reduce input costs and improve resource efficiency. However, uneven access to digital infrastructure, investment capital and technical skills continue to constrain digital adoption in agriculture, reinforcing disparities between digitally enabled farms and more traditional operations.

Current State of Technology Adoption in Italy’s Traditional Farms

Italy’s agricultural sector presents a mixed and uneven picture when it comes to digital transformation in agriculture. On one hand, the country is considered among the more active European markets in precision agriculture development. The Smart Agrifood Observatory of the Politecnico di Milano and the International Center for Sustainable Development (often referenced in sector reports), have highlighted steady growth in the adoption of precision agriculture development, farm management software and data-driven technologies, particularly among medium and large-scale enterprises leading the shift toward Agriculture 4.0.

However, this progress coexists with significant structural disparities. Digital adoption in agriculture remains concentrated in more capitalized farms and in regions with stronger infrastructure and advisory ecosystems. Many small and traditional farms – which still represent the majority of holdings in Italy – face constraints related to investment capacity, digital skills, and connectivity.

As a result, Italy’s position as an innovator in certain segments of smart agriculture does not fully reflect the uneven diffusion of digital tools across the broader farming landscape. This imbalance illustrates the persistent digital divide in agriculture affecting traditional operations.

Regional Disparities in Digital Access

Geographic location plays a significant role in shaping technology access and farm digitalization adoption across Italy. Available data from sector observatories and regional reports consistently show higher uptake of precision agriculture technologies in Northern regions compared to Central and Southern Italy. The Northeast and Northwest concentrate a larger share of farms using precision Agriculture 4.0 solutions, digital farm management systems and connected machinery, while adoption rates remain comparatively lower in Southern regions and in more remote inland areas.

Although exact percentages vary depending on methodology and sample (and are not uniformly confirmed across official national statistics), the broader pattern is clear: Northern Italy benefits from stronger infrastructure, higher average farm capitalization and more developed advisory ecosystems, all of which facilitate digital adoption in agriculture.

Connectivity represents an additional structural divide. According to recent ISTAT and Eurostat data, internet access among households in rural areas in Italy remains lower than in urban areas, though the gap has narrowed in recent years. Rural household Italy connectivity rates are typically several percentage points below national averages, and high-speed broadband coverage is uneven — particularly in mountainous, inland and sparsely populated zones.

In agricultural terms, connectivity challenges are more acute in heterogeneous rural landscapes, including hilly and mountainous areas, permanent crop zones and non-irrigated arable land located far from urban centers. Limited broadband coverage in these areas can constrain the use of real-time data systems, cloud-based farm management tools, and connected machinery. By contrast, farms located in more accessible and infrastructure-rich areas face fewer connectivity barriers.

Regional policy implementation further influences adoption dynamics. While digitalization is a stated priority within the Common Agricultural Policy (CAP) Strategic Plan and regional Rural Development Complement programs, the intensity and speed of activation of digital-focused measures vary by region. In some areas, limited advisory services, training programs, and targeted investment schemes reduce farmers’ ability to access and implement digital adoption in agriculture.

Overall, Italy’s digital divide in agriculture reflects a combination of infrastructure gaps, structural farm characteristics and uneven regional policy execution rather than a purely technological lag.

Gaps Between Large Commercial and Small Traditional Farms

Farm size remains one of the most decisive factors in digital and precision agriculture adoption in Italy. Multiple sector analyses show that larger farms are significantly more likely to adopt precision agriculture tools, connected machinery and Agriculture 4.0 technologies than smaller holdings.

While precise adoption rates vary by survey and year, data consistently indicate that farms managing over 100 hectares show substantially higher uptake of precision technologies compared to small farms under 50 hectares. Medium-sized farms (50–100 hectares) tend to fall in between. The structural pattern is clear: adoption probability increases with farm size and capitalization.

The economic rationale is straightforward. Larger farms can distribute the fixed costs of digital equipment – such as GPS-guided machinery, sensors, data analytics platforms and variable-rate technologies – across a broader acreage base. This improves return on investment through input savings, operational efficiency, and labour optimization.

Access to financial support further influences adoption. Investment incentives under the Common Agricultural Policy (CAP), national “Agriculture 4.0” tax credits and regional funding schemes have played a significant role in accelerating digital uptake. Survey data from recent years suggest that a substantial majority of farms investing in Agriculture 4.0 solutions benefited from at least one form of public incentive. This underscores how targeted financial support can drive accelerated agricultural technology adoption.

By contrast, smaller farms – particularly those located in less favored or marginal areas – often face greater barriers to accessing credit, co-financing requirements and technical advisory services. For these operations, high upfront investment costs and uncertain payback periods can slow or prevent adoption, reinforcing structural disparities within the sector.

Ultimately, scale affects not only cost efficiency but also risk tolerance, investment capacity and access to support ecosystems, all of which shape the digital divide between large commercial enterprises and smaller traditional farms.

Statistics on Connectivity and Tool Usage

National data on digital agriculture adoption in Italian agriculture often appear contradictory because they measure different dimensions of technology use.

On the one hand, a significant share of Italian farms report using at least one form of digital tool, which may include basic farm management software, digital accounting systems, GPS-enabled machinery or online administrative system. This suggests that digital technologies are no longer purely experimental within the sector.

On the other hand, when looking specifically at advanced Agriculture 4.0 and precision farming technologies, penetration remains far more limited. Estimates from recent sector observatories indicate that only a minority of farms have adopted integrated precision agriculture systems, and the share of utilized agricultural area managed with advanced digital techniques remains well below one-third of total land. Growth has been steady but incremental rather than exponential.

Digital maturity assessments further highlight structural disparities. A large proportion of farms – particularly small and family-run operations – remain at an early stage of digitalization, using isolated tools rather than fully integrated systems. Only a limited segment of larger, capital-intensive enterprises can be considered digitally mature, with connected machinery, data integration, and analytics embedded in operational decision-making.

Investment dynamics also reveal concentration effects. Public incentives, including Agriculture 4.0 tax credits and CAP-linked support measures, have stimulated technology uptake. However, evidence suggests that farms already positioned to invest – typically medium and large operations – capture a substantial share of these incentives. These risks widen the gap between digitally advanced enterprises and smaller farms that lack co-financing capacity.

Long-term structural data show gradual progress in farm computerization and connectivity over the past decade, with rural internet access improving significantly. Nevertheless, persistent weaknesses remain. Limited broadband coverage in remote areas, insufficient digital skills training and fragmented advisory services continue to constrain broader and more equitable adoption (digital divide in agriculture).

Geography further influences outcomes. Plains and highly mechanized production systems tend to integrate digital farm technologies more rapidly, while hilly and mountainous areas – where farms are smaller and production models more diversified – face additional barriers to cost-effective deployment of precision tools.

Overall, while digital agriculture in Italy is advancing, adoption remains uneven across farm size, region and production systems.

Closing the Digital Divide in Agriculture

Main Barriers Preventing Digital Adoption

Despite steady progress in digital transformation in agriculture, multiple structural barriers continue to limit adoption among traditional farms. These obstacles are rarely isolated; rather, they interact and reinforce one another, contributing to a persistent digital divide in agriculture across the sector.

Limited Internet Connectivity in Rural Areas

Infrastructure gaps remain a foundational driver of digital exclusion in agriculture.

According to the USDA’s biennial Technology Use (Farm Computer Usage and Ownership) survey, about 85 % of U.S. farms reported internet access in 2023, leaving roughly 15 % without connectivity. Among farms with internet access, only about half reported using broadband as a connection type. While USDA statistics do not directly measure “insufficient connectivity for advanced tools,” these figures indicate that a meaningful share of farms lack robust internet infrastructure. At the national level, Federal Communications Commission data show that rural Americans are disproportionately likely to lack broadband meeting the historical 25 Mbps download / 3 Mbps upload benchmark: approximately 17 % of rural residents lacked access at that standard in recent reports, compared with about 1 % of urban residents, underscoring the persistent rural–urban digital divide.

The economic logic behind this disparity is well established. Extending high-speed broadband infrastructure across sparsely populated agricultural regions involves high capital expenditure and lower expected returns compared to dense urban markets. Terrain complexity – including mountainous areas, forests and large plains – further increases deployment costs for terrestrial fiber and fixed wireless systems. As a result, private investment alone has often proven insufficient without public subsidies.

GSMA (Global System for Mobile Communications Association) data show that while mobile broadband networks now cover the vast majority of the world’s population, coverage does not necessarily translate into usage. Nearly 96 % of people live within a mobile broadband footprint, yet an estimated 3.1 billion people remain offline despite coverage, a gap known as the “usage gap.” This gap is especially large in regions such as Sub-Saharan Africa, where more than half of the population lives within coverage but does not use mobile internet. The overwhelming majority of those who remain unconnected live in low- and middle-income countries, illustrating a global connectivity paradox where access to infrastructure coexists with low adoption due to affordability, skills and other barriers (rural digital divide).

Even where basic mobile broadband exists, rural areas frequently experience unstable speeds, limited bandwidth and insufficient fibre backbone infrastructure. These constraints restrict effective access to cloud-based farm management systems, real-time sensor monitoring, and data-intensive applications. Affordability also plays a role: the cost of devices, data plans, and maintenance can remain prohibitive for small-scale farmers.

Without reliable and affordable connectivity, many digital agriculture tools cannot function at full capacity. Infrastructure, therefore, remains a prerequisite for equitable farm digitalization across agricultural systems.

High Upfront Costs and Financial Constraints

Financial barriers consistently rank among the most cited obstacles to precision agriculture adoption of digital agriculture. Multiple international surveys – including those conducted in North America and Europe – indicate that high upfront costs and uncertain returns on investment are leading concerns for farmers considering precision agriculture and digital farm management systems.

While reported percentages vary by study, a substantial share of farmers in both regions identify capital expenditure as the primary constraint. Equipment upgrades, subscription-based software platforms, connectivity infrastructure, and data integration services require significant investment. For many farms, especially small and medium-sized operations, the financial risk associated with digital adoption in agriculture remains a decisive factor.

Uncertainty regarding return on investment (ROI) further slows adoption. Farmers often report difficulty in quantifying the economic benefits of digital tools, particularly where gains depend on scale, agronomic conditions or integration with existing machinery. In emerging markets, cost sensitivity is even more pronounced, with high upfront investment frequently cited as a primary adoption barrier in international development studies.

Machinery costs illustrate the scale of the challenge. Advanced combines, tractors and precision-enabled systems can cost several hundred thousand dollars, depending on specifications and embedded technologies. Even where farmers lease equipment or access shared machinery, services, maintenance, repairs and software upgrades add ongoing financial obligations.

Adoption patterns strongly correlate with farm size. Larger operations are more likely to invest in precision agriculture technologies because they can spread fixed costs across greater acreage, improving payback potential. Smaller farms, particularly those operating fragmented or diversified production systems, face tighter margins and reduced investment capacity. However, describing these barriers as “insurmountable” would be overstated; targeted financial incentives, cooperative models and scalable digital agriculture systems can mitigate cost constraints when properly designed.

Lack of Digital Skills and Training

Knowledge and skills gaps remain significant barriers to digital transformation in agriculture, even where infrastructure and funding mechanisms are available.

According to the GSMA, across low- and middle-income countries (LMICs), the primary barrier to mobile internet use among individuals who are aware of mobile internet services is limited literacy and digital skills. The GSMA Mobile Connectivity Index and annual State of Mobile Internet Connectivity reports consistently identify digital literacy, affordability and relevance as leading constraints. These barriers disproportionately affect women, particularly those with lower levels of formal education and income, contributing to a persistent gender digital divide.

At the farm level, research in both developed and developing contexts shows that lack of technical knowledge, uncertainty about the value of digital tools for farmers and limited access to skilled labour reduce adoption rates. While precise figures vary by study, surveys conducted in U.S. states and European regions indicate that farmers frequently cite insufficient knowledge about the economic value of digital agriculture technologies and difficulty finding qualified personnel to manage data-driven systems as major obstacles.

In many smallholder contexts, low levels of digital literacy further constrain digital adoption in agriculture. Access to smartphones or connectivity alone does not ensure effective use. Farmers may lack the skills required to navigate digital platforms, interpret agronomic data dashboards, or integrate decision-support tools into production practices.

Training and advisory services remain unevenly distributed. In several regions, formal education programs, extension services, and private-sector support mechanisms have not kept pace with the complexity of digital agricultural technologies. As a result, producers often require targeted capacity-building initiatives – including hands-on technical training and peer-learning networks – to effectively adopt and benefit from digital tools.

Overall, digital infrastructure without human capital development risks deepening the digital divide in agriculture between technologically advanced farms and those lacking the skills to participate fully in digital agriculture systems.

Cultural Resistance to New Technologies

Socio-cultural factors play a significant role in shaping agricultural technology’s adoption, particularly in small-scale and traditional farming systems. Development research and rural sociology literature consistently show that digital transformation in agriculture decisions is not purely economic; they are embedded in social norms, community structures and value systems.

In many smallholder contexts – especially in parts of Sub-Saharan Africa and South Asia – farming practices are closely tied to kinship structures, gender roles, customary land tenure systems and intergenerational knowledge transmission. Land ownership and labour organizations may follow customary or collective arrangements rather than purely market-based models. These institutional frameworks influence investment decisions, risk tolerance, and openness to technological change.

Modernization-oriented technologies can sometimes challenge established systems. For example, precision agriculture, input-intensive crop systems, or contract farming models may emphasize individual property rights, market integration, and monocropping strategies. In communities where collective land management, mixed cropping systems or shared labour structures dominate, such transitions can generate hesitation or resistance.

Empirical studies document how religious beliefs, traditional authority structures and customary norms influence farming decisions. In some rural communities, agricultural activities are linked to spiritual practices or regulated by customary calendars. Decisions about adopting new crop varieties, inputs or mechanization may involve consultation with family elders or community leaders. While these dynamics vary significantly across regions and ethnic groups, they illustrate how digital adoption in agriculture is socially negotiated rather than purely individual.

Importantly, describing these dynamics as “innovation resistance” can be misleading. In many cases, farmers are engaging in rational risk assessment within culturally embedded systems. Established agricultural practices provide stability, social legitimacy, and resilience in uncertain environments. New technologies introduced without alignment to local institutions, knowledge systems, or trust networks are less likely to diffuse successfully.

Research in farming technologies innovation systems increasingly recognizes that effective digital transformation requires participatory approaches, culturally sensitive extension services, and locally adapted business models. Farming Technology adoption succeeds most sustainably when it complements – rather than displaces – existing social and institutional structures.

Proven Strategies to Support Traditional Farms in Digital Transition

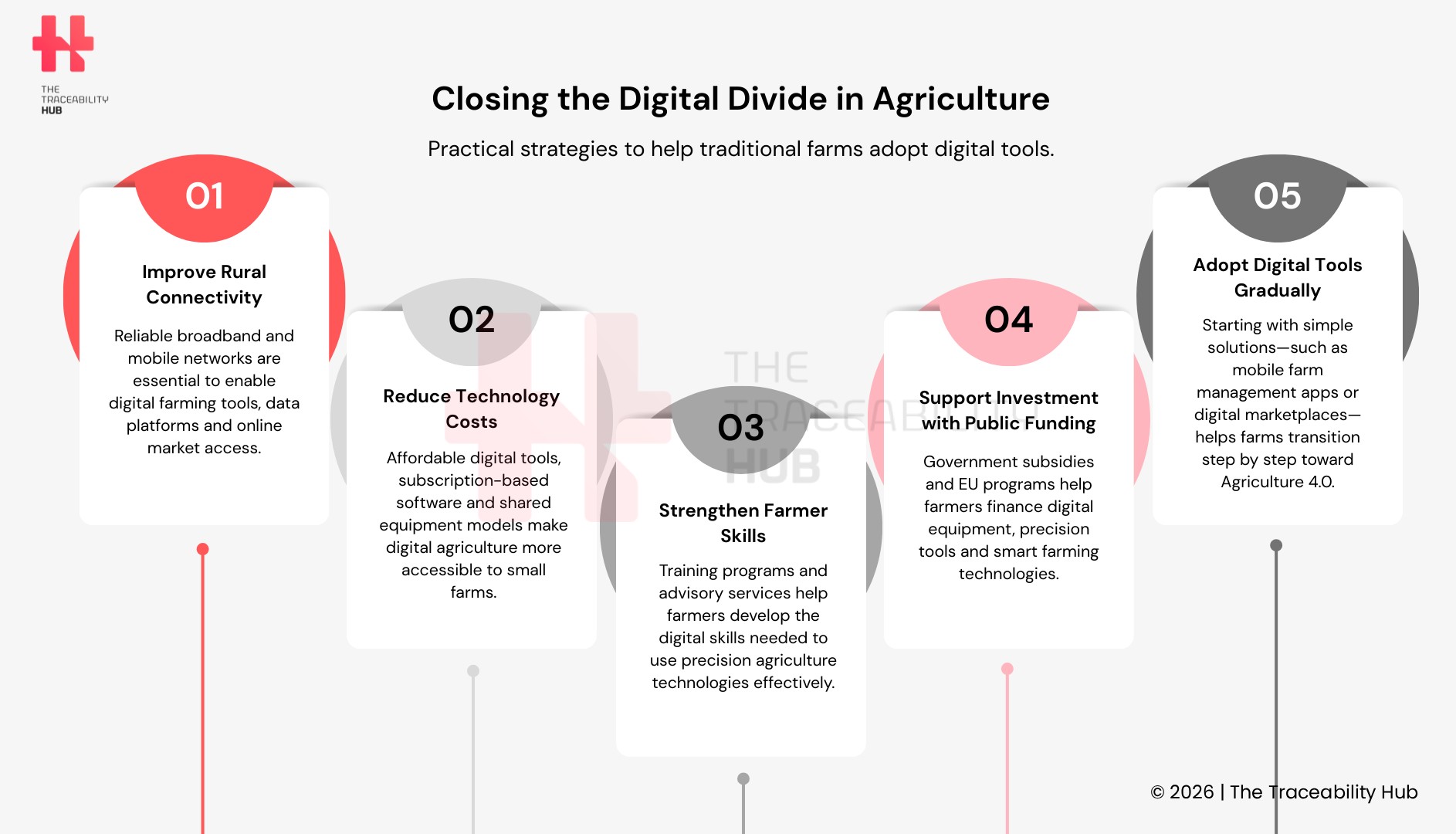

Closing the digital divide in agriculture requires coordinated and evidence-based action. International experience shows that traditional farms benefit most from integrated strategies that simultaneously address financial constraints, infrastructure gaps, and knowledge barriers.

Rather than relying on isolated technology deployment, successful approaches combine public investment in rural connectivity, targeted financial incentives, farmer training programs, and cooperative adoption models. When infrastructure, affordability and skills development advance together, farming digital tools are more likely to generate measurable productivity and resilience gains.

While outcomes depend on local institutional capacity and market conditions, policy experience across Europe, North America and emerging economies demonstrates that structured, multi-dimensional strategies can significantly reduce barriers to digital adoption in agriculture.

Affordable and Shared Technology Solutions

The cost structure of digital agriculture technologies has evolved significantly in recent years, making certain tools more accessible to small and medium-sized farms.

Many farm management software providers now operate on subscription-based or freemium models, lowering upfront capital requirements. Basic livestock tracking, record-keeping, and compliance management functions are often available through tiered pricing structures, enabling smaller producers to adopt digital tools in agriculture without large initial investments.

Digital agriculture technologies and hardware costs have also declined in specific segments. Entry-level soil moisture sensors, weather stations and GPS guidance systems are now available at substantially lower prices than a decade ago, partly due to advances in Internet of Things (IoT) technologies and increased global manufacturing scale. While high-precision, integrated farming systems remain expensive, modular and lower-cost devices can still provide actionable agronomic data for irrigation scheduling, planting optimization and input management.

Drone technology has followed a similar trajectory. Consumer and prosumer-grade drones suitable for crop monitoring are significantly more affordable than early-generation agricultural UAV systems. However, advanced multispectral or spraying drones remain capital-intensive, and regulatory requirements can add additional costs.

Remote farming monitoring systems have also benefited from falling hardware prices and the expansion of cloud-based platforms. Subscription-based farm management software reduces the need for on-site IT infrastructure, enabling live monitoring of livestock conditions, machinery performance, and water systems. That said, reliable connectivity and ongoing subscription fees remain necessary components of total cost.

Importantly, shared service models – including cooperatives, machinery rings and service providers offering “technology-as-a-service” – further lower financial barriers. Instead of owning equipment outright, smaller farms can access precision agriculture services through contractors or collective ownership structures.

In summary, while digital agriculture technologies are not universally inexpensive, market evolution, modular design, and shared-service models have lowered entry barriers compared to earlier phases of adoption.

Cooperative Models for Equipment Access

Equipment sharing models address a fundamental structural reality: farm machinery is typically one of the largest capital expenses after land acquisition. Tractors, combines and precision-enabled farming technologies require substantial upfront investment and ongoing maintenance costs, creating financial barriers for small and medium-sized farms.

Across Europe and North America, cooperative ownership and machinery-sharing arrangements have emerged as practical farming solutions. These models allow farmers to pool capital, share depreciation costs, and improve asset utilization rates.

France offers the most established example. The country has more than 12,000 agricultural machinery cooperatives known as Coopératives d’Utilisation de Matériel Agricole (CUMA). These cooperatives involve roughly one-third of French farms and are widely recognized as a scalable model for collective investment in agricultural equipment. CUMA models structures enable members to access machinery – including high-cost precision technologies – at significantly reduced individual cost compared to sole ownership.

In Scandinavia, Germany and other EU Member States, machinery and equipment cooperatives have similarly demonstrated cost efficiencies. Academic studies indicate that shared-use arrangements can reduce per-unit machinery costs through higher utilization rates and lower idle time, though savings vary depending on coordination efficiency and scheduling flexibility.

In the United States, informal equipment-sharing groups, LLC-based cooperatives and grant-supported initiatives also operate at local levels. While specific savings percentages vary by case, the economic rationale is consistent: spreading fixed machinery costs across multiple farms lowers capital burden and reduces financial risk, particularly for small-scale producers (support small farm competitiveness).

Equipment sharing is not without challenges. Coordination, scheduling conflicts, and maintenance responsibilities can reduce efficiency gains. However, when governance structures are clear and member participation is strong, well-governed cooperative models can significantly lower entry barriers to mechanization and precision agriculture technologies.

Government Subsidies and EU Funding Programs

Public funding plays a central role in accelerating digital agriculture adoption.

In the United States, the United States Department of Agriculture (USDA) administers major conservation and innovation programs, including the Environmental Quality Incentives Program (EQIP) and the Conservation Stewardship Program (CSP). While these farming programs primarily support conservation practices, they also fund precision agriculture tools that improve resource efficiency. Annual funding allocations for this digital transformation in agriculture programs reach billions under the Farm Bill framework, although digital adoption represents only a portion of supported activities.

Innovation-focused funding mechanisms, including research programs under advanced agricultural innovation initiatives, aim to support next-generation technologies that reduce chemical inputs and enhance sustainability.

In the European Union, the European Commission’s Horizon 2020 program funded numerous research projects in digital transformation in agriculture and precision agriculture, spanning robotics, IoT, data platforms, and smart farming systems. Under the Common Agricultural Policy (CAP) 2023–2027, digitalization is embedded within national Strategic Plans through investment support, advisory systems (AKIS), and modernization measures. Rather than a single adoption target, CAP supports farm digitalization through integrated rural development funding instruments.

Open-Source Agricultural Tools

Open-source farming solutions offer cost-effective entry points for digital adoption.

- farmOS provides web-based farm management, planning and record-keeping software under an open-source license.

- LiteFarm is an internationally used open-access farm management platform supporting sustainable production systems.

- Farm Hack operates as a collaborative forum where farmers exchange designs and knowledge on low-cost, farmer-built tools.

These agricultural technology platforms reduce dependency on proprietary software ecosystems and lower financial barriers to experimentation.

Mobile-First Solutions for Limited Connectivity

Mobile-first digital platforms increasingly incorporate offline functionality to address connectivity gaps in low-bandwidth areas. Certain farm management applications allow users to store data locally and synchronize once internet access is restored. This approach enables task management, field mapping, and record-keeping in low-connectivity environments.

Tailored Training and Education Programs

Capacity-building initiatives complement infrastructure and funding efforts.

The World Bank and affiliated institutions provide online courses and knowledge resources covering digital agriculture technologies, mobile applications and digital advisory systems.

Workforce training organizations such as Palette Skills offer digital agriculture programs that introduce participants to GIS, IoT, drone technologies and AI applications for farmers. Program structures vary, but they are designed to build practical digital competencies for agricultural innovation.

Real Success Stories from Italian Traditional Farms

Across Italy, case studies illustrate how traditional farms are integrating digital tools to address structural constraints such as market access, resource efficiency and operational management.

Research from sector observatories and agricultural associations highlights examples of small and medium-sized producers adopting precision irrigation systems, farm digitalization and digital traceability platforms, smart viticulture monitoring tools and direct-to-consumer e-commerce solutions. These initiatives demonstrate how incremental and context-specific technology adoption can improve competitiveness without fundamentally altering farm identity or production models.

Rather than eliminating all structural barriers, these examples show how targeted digital integration in agriculture – supported by advisory services, public incentives and cooperative models – can narrow elements of the digital divide. They provide replicable frameworks for other traditional farms seeking to modernize while preserving product quality and territorial value.

Small Vineyard Digital Transformation in Viticulture

In regions such as Tuscany, precision viticulture increasingly relies on satellite imagery and remote sensing technologies to monitor grapevine vigor, water stress, and disease risk. Using vegetation indices derived from satellite data, vineyards can identify variability across parcels and intervene selectively rather than applying uniform treatments.

These digital agriculture systems detect stress patterns that are not easily visible to the human eye, allowing targeted pruning, irrigation adjustments or plant protection treatments before issues escalate. When integrated with weather forecasting and disease-risk models, satellite monitoring can support more precise and potentially reduced chemical applications.

Rather than blanket interventions across entire vineyards, producers can treat specific rows or zones. This digital agriculture approach aligns with the core principle of digital agriculture: data-informed decision-making aimed at improving resource efficiency, sustainability, and product quality.

Precision Agriculture in the Olive Sector

The olive oil sector faces structural pressures including rising production costs, labour shortages, water scarcity, and increasing climate variability. Digital technologies for farmers are being introduced to address these challenges.

Precision agriculture tools – such as soil moisture sensors, remote sensing, weather-based disease forecasting models and digital farm management systems support more efficient irrigation scheduling and pest management. In some contexts, machine learning models are used to analyze agronomic data and improve decision-making.

Advanced agriculture monitoring systems can contribute to improved resource efficiency and more consistent quality control. When combined with digital traceability platforms, these technologies also strengthen transparency and product authenticity in olive oil supply chains, an important factor in fraud prevention and consumer trust.

While agricultural technology adoption levels vary, precision tools offer measurable operational improvements where infrastructure and training are available.

Family Farm E-Commerce Transformation

Farm digitalization extends beyond field technologies to include market access. Several family-run agricultural businesses have successfully integrated e-commerce into traditional operations.

For example, Perfect Plants Nursery – a long-established plant nursery in the United States – transitioned toward a strong direct-to-consumer online model and reported multimillion-dollar annual revenues following its digital expansion.

Similarly, many small and medium-sized farms adopt direct-to-consumer e-commerce platforms to report significant sales growth after integrating online storefronts and digital marketing strategies. These cases illustrate how digital agriculture adoption can strengthen revenue resilience by reducing reliance on intermediaries and expanding geographic reach.

E-commerce demonstrates that the digital divide in agriculture is not limited to precision tools in the field. It also encompasses access to digital markets, branding, logistics, and consumer engagement.

Creating Your Farm’s Digital Adoption Roadmap

Digital transformation in agriculture requires structured planning rather than isolated technology purchases. International policy frameworks and agricultural innovation systems increasingly emphasize phased, strategic adoption approaches.

A digital agriculture adoption roadmap enables farmers to move from broad intentions to actionable steps. It typically begins with an assessment of current operations – including infrastructure, skills, production systems, and financial capacity – before identifying technologies aligned with specific operational goals.

Rather than adopting farming digital tools opportunistically, a roadmap supports sequential implementation: piloting selected technologies, evaluating return on investment and integrating solutions into existing workflows. This structured approach reduces financial risk, improves user acceptance, and increases the likelihood of measurable performance gains.

By combining infrastructure readiness, training, advisory support and clear performance metrics, farms can approach digital transformation as a managed process rather than a disruptive leap.

Checking Your Current Technology Baseline

Effective digital adoption begins with a structured readiness assessment. International agricultural development frameworks recommend starting with a diagnostic phase that evaluates existing infrastructure, connectivity, digital skills, financial capacity, and production systems.

A comprehensive assessment typically includes:

- Mapping the farm’s current technology use

- Identifying operational bottlenecks

- Evaluating connectivity and data management capacity

- Assessing workforce digital skills

Rather than assuming digital tools for farmers will automatically generate value, farmers benefit from identifying specific challenges where technology can improve productivity, efficiency, or sustainability.

Ranking Solutions Based on Farm Needs

Once readiness gaps are identified, potential digital use cases can be prioritized based on impact and feasibility. This structured approach helps farmers avoid overinvestment in complex systems before foundational farming tools are in place.

Starting with relatively simple digital tools for farmers — such as mobile-based record-keeping, task scheduling or weather forecasting apps — often provides immediate operational benefits and builds confidence in digital workflows. Selecting one or two digital farming technologies aligned with clearly defined objectives reduces implementation risk and financial exposure.

Finding Funding and Support Programs

Public support mechanisms can significantly lower financial barriers.

In the United States, the United States Department of Agriculture (USDA) Rural Development division provides loans, loan guarantees and grants to rural businesses and cooperatives. The Farm Service Agency also offers direct and guaranteed loans for beginning farmers who may not qualify for commercial financing.

In the European Union, digital investments can be supported through CAP Strategic Plans, rural development measures, and advisory services under Agricultural Knowledge and Innovation Systems (AKIS). Public programs can significantly reduce the cost burden associated with farm digitalization.

Building Skills Step by Step

Technology adoption requires parallel investment in human capital. Farmers can strengthen digital competencies through workshops, webinars, extension services, and advisory programs.

Structured farming digital transition initiatives — often delivered through agricultural extension networks, innovation hubs or rural advisory systems — guide participants through readiness assessment, agriculture platforms and technology selection and phased implementation planning.

Ongoing monitoring is essential. Farms should regularly evaluate technology performance, measure return on investment and adjust implementation strategies to optimize results over time.

Rethinking Digital Access in Italian Agriculture

The digital divide in agriculture separating many of Italy’s traditional farms from more technologically advanced operations is not inevitable. While structural constraints remain, evidence from cooperative equipment models, public funding mechanisms and modular digital tools demonstrates that meaningful progress is achievable through incremental and targeted action.

Collective ownership arrangements, investment support under national and EU frameworks, and mobile-first solutions designed for limited connectivity environments offer practical entry points for smaller producers operating under tight financial conditions. Case studies of digital agriculture Italy from precision viticulture and the olive sector illustrate how selective technology adoption — when aligned with clear operational goals — can improve resource efficiency, quality control and market positioning.

For traditional farms, the starting point is not farming technology acquisition but assessment. Identifying concrete operational needs before selecting digital tools reduces risk and improves return on investment. Entry-level solutions such as digital record-keeping applications or shared equipment participation can build capability and confidence without overwhelming financial or organizational capacity.

Digital transformation in agriculture rarely occurs through sudden disruption. It advances through structured, incremental steps. When supported by training, advisory services, and appropriate funding instruments, these steps can strengthen competitiveness and environmental performance over the long term.

Read more: Italy Fashion Certification 2026: New Textile Industry Rules & Supply Chain Compliance