CPG Industry: Inflation, Execution & Emerging Market Growth

The CPG industry (Consumer Packaged Goods) is a massive economic powerhouse that generated $7.5 trillion in global retail sales value in 2024, growing 7.5% from the previous year. Price increases, not volume growth, drove about three-quarters of these gains highlighting the ongoing post-inflation era challenges for manufacturers and retailers alike.

CPG products play a vital role in economic growth. These goods make up 20% of the US GDP and create jobs for more than 20 million Americans. The US CPG sector alone is worth about $2 trillion, and experts project the global industry will add $3.18 trillion in value during 2024. The picture isn’t all rosy though. The world’s 50 largest CPG brands by revenue grew just 1.2% in the first half of 2024, indicating that top-tier brands lag smaller challenger brands and the broader market.

This piece looks at the changing world of consumer-packaged goods. We’ll explore current market trends, what’s driving regional growth, how consumer behaviors are shifting, and the ways digital innovation and AI are altering the map for CPG brands worldwide.

Global CPG Market Outlook for 2025

The consumer-packaged goods industry’s retail sales continue to grow, though at a slower pace than before. Market patterns suggest CPG companies must adapt their strategies to grow in 2025.

Retail Sales Value Trends: 2022–2024

The global CPG industry has shown remarkable strength over the last several years. The retail sales value (RSV-driven markets) grew by 9.8% in 2022 and 9.3% in 2023. The market reached an estimated $7.5 trillion with a 7.5% year-over-year increase in 2024. This gradual slowdown points to normalization after the post-pandemic boom. The current growth rate still doubles the 10-year industry average, which suggests continued strength.

Food and nonalcoholic beverages slowed down more noticeably in 2024. These categories raised prices a lot throughout 2023. The growth moderation varied between product categories. Essential items outperform discretionary segments.

Analysts expect 3-5% growth in 2025 after adjusting for inflation. This rate is about half of what we saw during pre-pandemic years. Global CPG growth will spread evenly across regions in 2025. China’s share will drop from over 30% to about 14% of global CPG volume growth.

Volume vs. Price Contribution to Growth

A deeper look at growth drivers reveals an important imbalance. Price increases drove about three-quarters of sales growth in both 2023 and 2024, rather than actual volume gains. This shows improvement from 2023, when prices factored in 90% growth, but still exceeds pre-pandemic levels underscoring inflation-driven consumer behavior shifts.

Developed markets show an even starker contrast. Price hikes generated 95% of revenue growth in 2023. Americans spent 10% more on groceries in 2023 but bought 4% fewer items. Developed markets achieved only 4.5% sales growth by 2024, down from 7.7% in 2023, with flat volumes.

Emerging markets generated almost all global volume growth. These regions saw 3% volume growth alongside their 11% year-over-year retail sales value increase in 2024. India stood out with nearly 15% RSV growth since 2022. This growth came from consumers switching from local products to international and premium brands.

Impact of Inflation on Developed Markets

Consumer behavior in developed economies has changed drastically due to inflation. US and EU prices rose more than 20% above first quarter 2020 levels by late 2024. This ongoing pricing pressure created “K-curve demand” – premium brands grow among wealthy consumers while mass-market products see falling demand.

CPG companies handled inflation well at first. US shelf prices jumped about 30% since 2020, outpacing the roughly 25% increase in CPG-delivered costs. The situation changed by 2023. Consumers became more price-conscious, brand loyalty weakened, and private labels/store brand gained market share. US consumers focused on value-oriented products. They chose either cheaper private label options or premium segments with clear benefits, which hurt the middle market.

US inflation should ease to just above 3% in 2025. Supply chain issues will likely continue to affect raw material costs, labor, and logistics. Even with some relief from inflation, shoppers will stay price sensitive as they remember pre-inflation prices. About 54% of CPG (Consumer Packaged Goods) leaders believe price increases won’t drive revenue growth in 2025. They think such increases would face retailer resistance and reduce consumer demand significantly.

The Evolving CPG Industry

Emerging Markets as Growth Engines

The global CPG market shows emerging economies leading the charge as vital growth catalysts. While mature markets rely on price increases for revenue growth, developing regions show healthier expansion through both value and volume growth. This trend has changed how CPG (Consumer Packaged Goods) companies plan their global strategies.

11% Sales Growth in Emerging Economies

The momentum in emerging markets reached new heights in 2024. These markets posted an 11% year-over-year increase in retail sales value, which was more than double the growth rate in developed markets. Double-digit growth has become a consistent pattern in these regions over the last several years. Global private consumption will likely double in the next decade, jumping from USD 65.00 trillion in 2025 to USD 110.00–120.00 trillion by 2035. The Asia-Pacific markets will propel most of this growth.

Multinational CPG giants hold strong positions in mature markets and Latin America but lag in high-growth regions like Asia, Africa, and the Middle East. These territories offer two powerful growth drives: population expansion and middle-class growth that wants branded goods. The Coca-Cola Company’s 2025 CAGNY presentation shows how industry leaders are responding – they now put emerging countries first.

The Asia-Pacific region stands out with digital sales growing faster than physical retail. The global CPG (Consumer Packaged Goods) market will likely grow by USD 1.50 trillion between 2024 and 2029, at a yearly rate of 4.9%. E-commerce sales, direct-to-consumer brands, urbanization, and higher disposable incomes in emerging economies are driving this expansion.

Volume Growth in India and Southeast Asia

Emerging Asian markets achieve balanced growth, unlike developed markets that rely on price increases. The Asia-Pacific region saw FMCG value grow 4% in the year ending June 2025. Volume grew 2.8% while prices rose only 1.2%. North America and Western Europe showed lower growth rates, mostly from price increases.

India’s market performs exceptionally well. The country saw 7.2% value growth in 2024 and an impressive 13.7% in 2025’s first half. By 2030, India’s consuming class might reach 825 million people – a huge jump from today’s 340 million. Indonesia shows similar promise, with its consuming segment expected to grow from 120 million to 200 million people by 2030.

Southeast Asia’s CPG market, valued between USD 300-400 billion, could grow 3-5% yearly over the next five years. This makes it one of the best growth opportunities worldwide. Food and beverages lead this growth across Indonesia, Vietnam, the Philippines, Thailand, Malaysia, and Singapore. Urban consumers with higher incomes are buying more premium products like health-focused nutrition, beauty, and skincare.

The region’s performance varies widely. Growth in Southeast Asia slowed to 1.8% in 2025’s first half, down from 3.5% in 2024. The ASEAN-5 countries should grow around 4.5% through 2030, with Indonesia leading the pack.

Deflationary Pressures in China’s Online Channels

China presents a mixed picture among emerging markets. After slow growth in 2024, early signs of recovery appeared as overall growth rose from 2.8% in 2024 to 4.7% in 2025’s first half. Online channels drove most of this improvement. However, consumer prices fell again in September as demand stayed weak.

The national consumer price index dropped 0.3% compared to last year, surprising market watchers. Weak domestic demand and oversupply continue to cause deflation. Lower food and energy prices played a key role in this decline.

The online CPG sector faces ongoing challenges. Weak consumer confidence and fierce price competition in e-commerce have created constant downward pressure on prices, even as volume grows. Traditional market channels still handle 70-80% of trade, but e-commerce platforms gain more influence.

Consumer Behavior Shifts in the Post-Inflation Era

Consumers worldwide have developed unique buying habits such as inflation, and the post-inflation era changes how they spend money. Their biggest worry remains rising prices, which ranks higher than global climate change and job security across all 18 markets in the survey.

Value vs. Premium Segment Dynamics

The way people assess their purchases has changed because of global inflation and rising costs in the CPG industry. Research shows 79% of consumers are spending less, but they’re not just buying fewer items or shopping at discount stores. They’ve become smarter about their conscious spending. More than half now search for deals on everything they buy, while 49% of US shoppers plan to wait before making purchases in the next three months.

What’s interesting is how people now make strategic trade-offs between different categories in their consumer behavior patterns. During early 2025, one-third of shoppers cut back in some areas while spending more on others. Even more surprising, 19% of people worldwide plan to reduce spending on necessities so they can buy more luxury items.

This split behavior has created what experts call “K-curve demand” – both premium and value segments grow while the middle market shrinks. US shoppers now put their money toward products they believe give them the best value, whether it’s cheaper to store brands (private label growth) or high-end premium items.

Discount and wholesale stores attract people from every background. The numbers show 80% of US Gen Zers shopped at wholesale clubs last month. Some buyers prefer smaller packages that cost less, while others save money by buying in bulk at stores like Walmart or Costco.

Private Label Growth in the US and EU

Store brands have changed dramatically alongside these new consumer behavior shifts. People no longer see them as just cheaper options – they’ve become popular choices as shoppers discover the quality and variety retailers provide.

Store brands dominate European CPG markets, with a 39% value share and 47%-unit share. Spain and France show particularly strong growth. British supermarkets lead the pack, with store brands making up nearly 60% of sales.

US store brand growth keeps picking up speed, though it’s still catching up with Europe. These brands now hold 22% of value and 24% of unit share. Sales grew steadily through 2022, rising 11.3% by December. Looking ahead, 54% of shoppers say they’ll buy more store brand products indicating sustained momentum in consumer-packaged goods retail sales value (RSV).

This trend shows no signs of slowing – store brands keep growing even as inflation cools down. US shoppers trust these products more than ever, with 80% rating of store-brand food quality equal to or better than national brands. Nearly 90% believe store brands offer similar or better value.

GLP-1 Medications and Food Consumption Patterns

Health trends have started reshaping what people eat, beyond just price concerns. GLP-1 medications (used for diabetes and weight loss), first created for diabetes but now used for weight loss, change not only physical health but also shopping habits.

A new nationwide study shows GLP-1 users have different food consumption preferences. People reporting less processed food consumption outnumbered those eating more by 70%. About 50% more users cut back on soda, refined grains, and beef compared to those who increased these items.

These changes show up in spending patterns too. A newer study, published in 2024, found that GLP-1 (used for diabetes and weight loss) users reduced their caloric intake by 21% while spending 31% less on groceries. Only fruits, leafy greens, and water consumption increased among users.

Big food companies have started adapting to these world consumers’ changes. Nestlé launched its first new brand in almost 30 years specifically for GLP-1 users, while General Mills and Danone now market high-protein and high-fiber products for health-conscious consumers to this growing market trend.

Challenges Facing Top CPG Companies

Big consumer packaged goods (CPG) companies are struggling financially in today’s complex market environment. The tough business climate of 2024 has hit the largest consumer goods manufacturers hard and exposed deep flaws in their traditional growth strategies.

1.2% Revenue Growth Among Top 50 CPGs

Leading global CPG brands aren’t doing well financially. The top 50 global CPGs by revenue grew just 1.2% year-over-year in the first half of 2024. Small challenger brands are doing much better and now capture up to 40% of total US consumer product growth.

Most of this modest growth comes from price increases rather than selling more products (volume growth). CPG sales have grown 4% on average since 2019. Price hikes account for over 90% of this growth, while actual sales volume dropped by 1.4 percentage points. This shows some serious problems:

- Market delays can threaten sales

- Poor data management and forecasting lead to high costs

- Programs meant to reduce complexity don’t work

- People resist price increases during high inflation

About 68% of the world’s biggest CPG makers haven’t bounced back to their pre-COVID profit levels when comparing the first half 2025 to 2019. Sales have dropped by 61% of the top FMCGs compared to last year.

Declining EBIT Margins vs Pre-COVID Levels

The complete profit picture for 2024 is still taking shape. Top CPG companies worldwide seem to have better earnings before interest and taxes (EBIT) margins in the first half, thanks to lower input costs. Yet these margins still lag pre-COVID levels for two reasons: supply chain problems still affect some raw materials and selling; general, and administrative (SG&A) costs keep rising.

Three out of four top 25 Fortune 500 CPGs companies haven’t reached their pre-COVID margins, despite trying various cost-cutting programs. Companies scrambling for growth while trying to cut costs have changed the industry’s profit-and-loss landscape.

Return on invested capital (ROIC) without goodwill reached 27%, up 400 basis points from before, while SG&A dropped 250 basis points. These numbers look good but hide deeper problems. Raw material prices are still 20–40% higher than in 2019 and will likely stay high until at least 2025.

Shareholder Return Trends: 5-Year Analysis

The stock market has noticed these struggles and uncertainties about future growth. The five-year shareholder returns for the biggest CPGs have dropped by more than half. Investors are worried about growth that relies too heavily on price increases, leading to lower margins and weaker stock performance.

This leadership crisis has hit companies hard financially. CPG companies have fallen from market darlings to poor performers in total shareholder returns across all sectors. They now lag other consumer-facing industries like tech, financial services, healthcare, and retail, which have done a better job of using digital technology to improve their business models and customer experience.

These CPG companies need to grow 4–5% yearly with 15–16% EBITA margins to become top performers again. This means growing 100–200 basis points faster than market predictions while pushing EBITA 100–200 basis points above current levels.

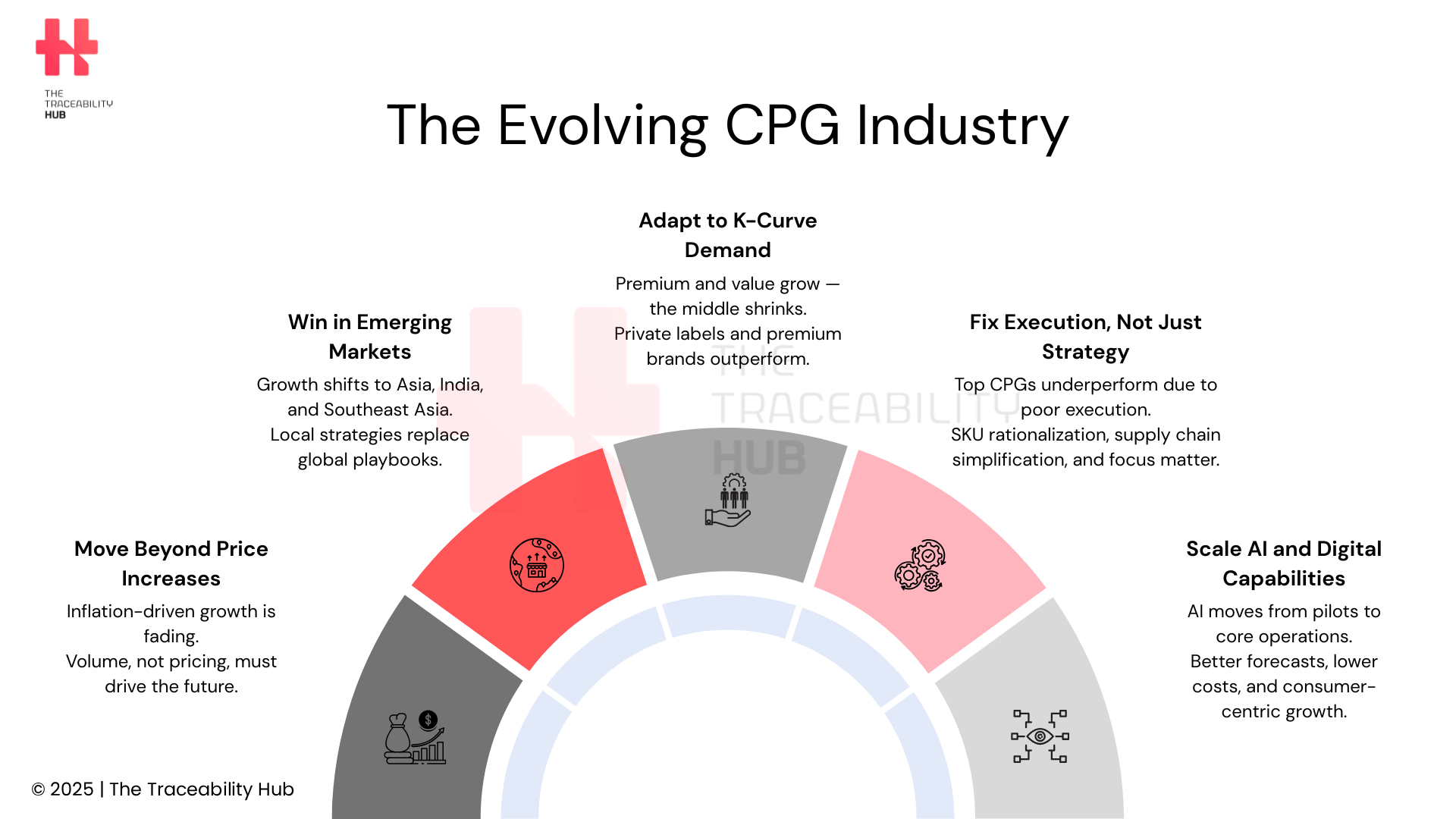

Rethinking the CPG Growth Algorithm

Traditional CPG growth models no longer work well. Progressive CPG organizations are creating new ways to grow. Successful companies go beyond cost management. They balance excellent execution, smart portfolio choices, and localized strategies for emerging markets.

Superior Execution in Mature Markets

Execution has become the biggest driver of growth for CPG companies. It now matters more than market momentum and mergers. Recent analysis shows that execution creates a 5.0 percentage-point difference in organic growth for top performers. This reality stands out clearly: excellent execution gives companies their main competitive edge in developed markets where volume growth remains hard to find.

The best companies focus on predicted growth—an analytical, consumer-focused approach that follows three steps: predict, transform, and sustain model. This model needs a strong focus on five execution areas:

- Agile innovation deployment — Leading CPG companies use lean digital innovation models. They test and learn quickly to catch new trends. The best ones launch innovations within months instead of years.

- Omnichannel optimization — Successful brands look closely at growth opportunities across channels. They invest heavily in digital commerce, direct-to-consumer strategies, and increasingly, eB2B solutions to help traditional partners digitally.

Live analytical insights have produced measurable results. Companies using AI for sales and demand planning and forecasting accuracy see 2% better return on investment and 5-10% more accurate forecasts.

Portfolio Expansion via M&A and Innovation

Portfolio expansion through smart M&A and genuine innovation has become crucial for slow-growing developed markets. Yet innovation shows worrying trends—65% of new products are just updating rather than true innovations. This marks the highest level in 30 years, while 76% of yearly product launches fail.

Companies getting ready for the predicted M&A surge in 2025 need several abilities:

The best buyers keep a clear M&A strategy that their C-suit agrees on, whether they buy from small companies or make big deals. They run comprehensive due diligence across all parts of the organization. They stay focused on value throughout the deal.

Creating new products needs a complete rethink:

- Consumer insights must evolve by combining AI-powered trend scanning with deep human insights from behavioral sciences

- Companies need an entrepreneurial culture that welcomes quick learning and failing

- Innovation should fit into the broader portfolio strategy, with resources spread across different types

Localized Strategies for Emerging Markets

Markets that were once global now fragment. CPG companies need fresh approaches to grow in emerging economies. These markets should generate about three-quarters of industry growth by 2028.

Success in new markets starts with understanding local patterns. Companies must assess market size, analyze consumer segments, map market competition, and evaluate regulations. This knowledge helps create specific approaches for each region instead of using one global strategy.

Local cultural understanding makes a big difference. Companies must respect local customs, create marketing that speaks to local people, and adjust products to match regional tastes (marketing and product adaptation).

Finding reliable distribution channels with partners helps companies enter markets smoothly and reach more customers. Some companies mix global brand power with local partnerships well, like Kellanova in Africa, where its Pringle brand works alongside local snacks and instant noodles made through joint ventures.

Smart localization brings big financial rewards. Southeast Asian consumer markets alone are worth USD 300–400 billion. They should grow 3-5% yearly over the next five years, making them one of the best global opportunities.

Reinventing for Continuous Productivity Gains

CPG companies (Consumer Packaged Goods industry leaders) need to achieve productivity gains of at least 5% yearly throughout their organizations to become profitable again in a tough market. What used to be occasional improvement initiatives have evolved into a core operating philosophy. Companies now look beyond quick fixes to find lasting supply chain simplification, SKU rationalization, and operational efficiency improvements.

SKU Rationalization and Margin Impact

Product complexity costs CPG manufacturers dearly. Food-and-beverage manufacturers lose about USD 50.00 billion in gross profit in the US market alone due to complexity. Smart SKU rationalization strategies remove underperforming products and deliver real benefits. Companies can boost their sales growth by 2 to 5 percentage points and improve margins by 100 to 400 basis points.

Recent success stories prove these benefits. A US-based packaged-food producer managed to keep its overall SKU count steady while removing ten low-volume products. The company added carefully selected new items to fill gaps in their product line and portfolio gap. This strategy projects over USD 50.00 million in run-rate gross margin improvements across five brands. Unilever’s CEO Hein Schumacher pledged to “lower complexity with over 20% reductions in SKUs, raw and packed materials and number of suppliers”.

Supply Chain Simplification with AI

AI and digital innovation now play a crucial role in streamlining CPG operations. Companies that use AI-powered supply chain management typically cut logistics costs by 15% and reduce inventory levels by 35%. They also see service performance improve by 65%. These gains come from smart forecasting and real-time optimization.

Real-world examples show AI’s value. PepsiCo uses automated order-building and dynamic truck routing. Mondelez’s AI-powered sales and demand planning led to a 2% better return on investment and 5-10% more accurate forecasts. Unilever’s AI system cut forecast errors by 10%, which substantially reduced stockouts and excess inventory, enabling better omnichannel optimization.

Divestment and Outsourcing of Non-Core Assets

Smart CPG leaders see the benefits of running lighter businesses. One global CPG company showed this by selling its home care brands that generated USD 2.50 billion in revenue. This move helped them focus on their main healthcare and hygiene categories. The strategic sales improved their focus and capital efficiency despite lower short-term revenue.

Companies explore new operational approaches beyond complete sales. They form strategic collaborations in warehousing, logistics, or manufacturing to gain flexibility and reduce fixed costs. This move toward lighter operations lets organizations focus their leadership, capital, and innovation on their strongest areas.

Market pressures push consumer and retail companies to keep streamlining operations. They sell non-essential assets, low-performing product lines, and units that don’t fit long-term goals. This strategy lets them reinvest in more profitable areas as margin pressure grows.

Redefining the AI-Led CPG Model

AI adoption is now a decisive factor for global CPG industry competitiveness. Today, 71% of CPG leaders use AI in at least one business function, a high increase from 42% in 2023. However, no organization has truly scaled these capabilities across their operations.

AI in Marketing Content Automation

Marketing departments are common starting points for AI tools adoption. We mainly see this because generative AI tools deliver quick wins with minimal barriers. Some CPG companies can now refresh over 100 product description pages in five minutes, a task that used to take weeks. These tools do more than save time. Organizations see a 21% improvement in search rankings from AI-optimized content. One beverage manufacturer used generative AI to create prompts, images, and concepts that shaped product development. This cuts their time-to-market by 60%.

ERP and Data Integration for Sales Execution

SAP’s phase-out of legacy systems has pushed more than two-thirds of leading CPG companies toward cloud-based platforms like S/4HANA. Smart organizations see this shift as a chance to reinvent their business models. Companies that combine AI with ERP systems improve their forecasting accuracy, reduce out-of-stock rates, and make better assortment decisions. Data fragmentation remains the biggest problem, CPG executives point to “breaking down data silos” as their main challenge to discover AI’s and digital innovation full potential.

Scaling AI Pilots Across Business Units

Research shows that generative AI applications could boost traditional AI’s economic effect by 15-40%. This could help CPG companies worldwide earn $160-270 billion more in annual profit. Yet this is just one piece of the puzzle, as traditional AI’s potential effect is 2.5-7.0 times larger than generative AI.

Companies that successfully scale AI share two key traits. They create AI councils to prioritize initiatives and provide ethical guardrails, and they carefully track concrete ROI measures. These companies quickly expand successful pilots across the business. They also place “AI champions”, users who are already comfortable with the technology, within business units to speed up adoption.

These steps support hyper-personalization, omnichannel optimization, and execution of excellence across the enterprise.

Building Consumer-Centric Digital Capabilities

CPG brands now put their customers–centric by using digital technologies and AI. This approach changes how people find and buy products. Brands don’t just adopt new technology – they completely change how they connect with their audience.

Hyper-Personalization in Product Discovery

Customer loyalty depends on hyper-personalization. Research shows that 80% of B2C customers value their company experience as much as the actual product. Companies that excel at personalization make 40% more revenue from their marketing than their competitors.

AI and machine learning help analyze how customers behave across different platforms. This knowledge helps brands offer relevant recommendations to their customers. A beauty brand, to cite an instance, used AI to create custom lipsticks on demand. This approach met customer needs and sped up marketing campaigns. Adidas saw similar success when their AI-driven personalization increased average orders by 259%.

This illustrates the potential of AI in digital innovation and loyalty-driven growth.

AI-Driven Meal Planning and Shopping Tools

People’s eating habits are changing, and AI-powered meal planning apps and tools are becoming popular. Cherrypick, an AI meal planning app, helps over half a million customers with custom recipes. The results show:

- 58% of users cook more from scratch

- 82% report better eating habits

- 70% eat more plant-based foods

The global personalized nutrition market will reach $38 billion by 2030. This is a big deal as it means that this sector has room to grow. About 40% of customers plan to use AI for product discovery within five years. Another 33% feel comfortable letting technology make purchases for them.

Digital Roadmaps for Long-Term Reinvention

CPG companies need solid planning instead of scattered digital projects. Recent surveys show executives are focusing more on AI and data capabilities, with a 24-percentage-point increase. Smart organizations create digital roadmaps that connect customer insights, technology, operational capabilities, and business objectives.

The numbers tell an interesting story. While 75% of executives think their organizations focus on customers, only 30% of customers agree. Companies must change everything from how they understand customers to how they make decisions. Only 15% of companies have a complete view of customer data and the right structure to use these insights effectively.

Global CPG Industry Transformation

The CPG (Consumer Packaged Goods) industry stands at a turning point as it faces major challenges while welcoming new opportunities. Price-driven growth, not volume growth, still dominates developed markets. This creates pressure on consumer loyalty and brand relationships that can’t last. India and Southeast Asia paint a different picture. These markets show balanced growth through both pricing and volume expansion, making them prime targets for strategic investment.

The post-inflation era has brought real changes in consumer behavior and how people buy. Premium and value segments are growing together, while mid-market products lose ground. This shows buyers are getting smarter about their choices. On top of that, private labels expansion has grown from basic alternatives into preferred choices. They now hold much of the market share across the US and the EU. These changes, plus health trends like GLP-1 medications that affect how people eat, mean manufacturers need fresh solutions.

Big CPG companies are struggling. The 50 largest global brands show a weak revenue growth of just 1.2%. They can’t keep up with smaller, more nimble competitors. Their shareholder returns have dropped sharply, pushing these former market leaders to the bottom quarter of performers across sectors.

Smart organizations know they need complete tech transformation. The foundations of new growth strategies include better execution in mature markets, smart portfolio growth, and local approaches to emerging economies. Companies also need to streamline processes through SKU reduction, AI-powered supply chain management, and selling off non-core assets to boost profits.

AI is without doubt the biggest driver of change in the global industry. It makes shared work possible at levels we couldn’t imagine before – from creating marketing content to improving ERP systems and connecting data. Companies that use AI throughout their operations see better forecast accuracy, fewer stock-outs, and better customer experiences.

Tomorrow’s winners will be companies that truly put customers first (customer-centric digital capabilities) and deliver unique experiences through digital tools. Those who welcome this change while tackling basic challenges like balancing price and volume growth will lead to the new CPG (Consumer Packaged Goods) world. Companies stuck in old ways risk falling behind as the industry reshapes itself.

Read more: How to Master Asset Tracking: Real Solutions for Real Businesses