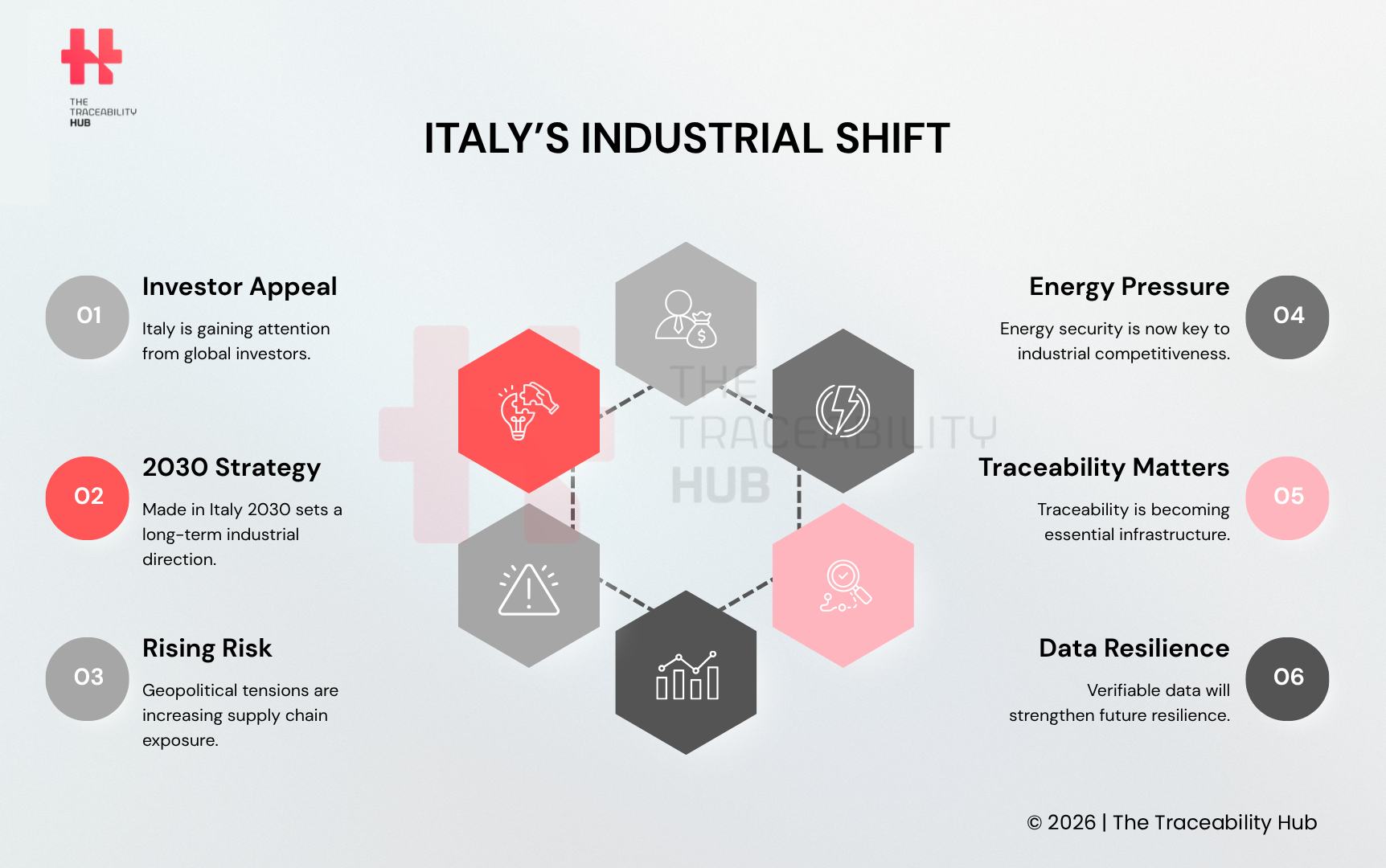

A New Phase of Attractiveness for Foreign Investment

Italy is entering a renewed phase of global economic relevance, marked by a gradual recovery in investor confidence and a re-positioning of its industrial system within an increasingly fragmented global economy.

After years of uncertainty, international capital flows toward industrial investment Italy-bound projects have shown renewed momentum, supported by a combination of industrial policy revival, modern infrastructure investment, and the broader reindustrialization is currently experiencing as a macro trend toward localized manufacturing resilience. While global foreign direct investment remains volatile, Italy has emerged as a comparatively stable and competitive destination within the broader European industrial policy framework.

This renewed attractiveness is reflected in Italy’s improved standing in the Global Attractiveness Index, where the country rose from 19th to 16th place in the most recent international ranking. According to the Index, the rise is linked to stronger industrial fundamentals, export capacity in high-value sectors, and increased capital formation, key highly valuable signals for long-term investors assessing European industrial structural competitiveness rather than short-term cost advantages.

What is changing is not merely the volume of Italy foreign investment, but the nature of Italy’s positioning. The country is no longer perceived solely as a traditional manufacturing hub; it is increasingly recognized as a strategic, evolving industrial system, one that combines specialized production, dense SME manufacturing networks, and policy-driven efforts to strengthen strategic autonomy Europe needs as a whole. In a complex global environment shaped by geopolitical supply chain risk, supply chain reconfiguration, and economic security concerns, this shift is becoming a decisive factor in capital allocation decisions.

“Made in Italy 2030”: A Systemic Industrial Strategy

For the first time in over three decades, Italy has articulated a comprehensive national industrial strategy. With Made in Italy 2030, the country formally returns to a centralized Italy industrial policy as a structural and long-term choice rather than a set of fragmented or emergency-driven measures.

The framework represents a clear structural shift in industrial governance. Instead of isolated incentives or sector-specific interventions, the overarching Italy industrial strategy is built around an integrated architecture that connects vision, objectives, and operational priorities across the production system. At its core are 18 industrial supply chains, spanning traditional areas of excellence and emerging domains, alongside enabling sectors critical to Italian manufacturing competitiveness.

A defining feature of modern manufacturing strategy – Made in Italy 2030 is its focus on governing four major transitions that are reshaping industrial economies globally: the digital transition, the green transition, the geopolitical transition, and the demographic transition. These core dimensions are not treated in isolation, but as interdependent forces that must be addressed through coordinated policy, targeted investment, and holistic data-driven industrial governance.

Within this framework, Italy’s manufacturing sector is explicitly repositioned as a central driver of economic growth, export capacity, and employment. At the same time, the strategy acknowledges that preserving Italy’s industrial base is not sufficient on its own: industrial modernization, operational scale, and technological upgrading are identified as essential to sustaining competitiveness in an increasingly contested global environment.

Particularly relevant is the strategy’s emphasis on an in-depth understanding of industrial supply chains. Identifying dependencies, strategic vulnerabilities, and value-creation mechanisms across European value chain production ecosystems becomes a prerequisite not only for effective public policy, but for industrial competitiveness itself. In an era of geopolitical fragmentation and economic security concerns, the ability to govern industrial interdependencies and strategic supply chain management emerges as a strategic asset.

Italy’s Industrial Shift

Geopolitical Instability and Supply Chain Exposure

Recent geopolitical instability supply chains in the Gulf region highlight a critical reality for global trade: global supply chain disruption risk is increasingly localized, yet its effects propagate along highly interconnected supply chains. Strategic chokepoints such as the Strait of Hormuz play a disproportionate role in global energy and commodity flows, making regional instability a global economic concern.

Italy’s direct trade exposure to the Gulf region remains relatively limited in terms of export and import volumes. However, this headline figure masks a more significant source of vulnerability regarding critical supply chain exposure. The country is deeply integrated into global production and logistics networks where disturbances in energy routes and upstream commodity markets translate rapidly into higher costs, supply uncertainty, and operational pressure across downstream industries.

Energy is a central element of this exposure. As a net energy importer, Italy is particularly sensitive to sudden global logistics disruption events and volatility in global oil and gas markets, especially when disruptions affect maritime transit routes critical to European supply. Even when physical supply is not immediately curtailed, price shocks and competition for alternative sources generate indirect but material impacts on industrial and manufacturing competitiveness.

Beyond energy, dependence on globally sourced industrial inputs, such as aluminum, chemicals, and other critical raw materials Europe relies on, represents a structural constraint and a constant commodity supply risk. These materials are essential for sectors ranging from manufacturing and packaging to mobility and energy transition technologies, yet they are not easily substitutable in the short term. Supply disruptions or price surges upstream can therefore translate into bottlenecks and margin compression downstream, increasing overall industrial risk exposure.

The key takeaway of how geopolitics affects industrial supply chains is that risk is no longer primarily macroeconomic or systemic. It has become sector-specific and supply-chain specific, shifting the focus from aggregate resilience to real-time supply chain monitoring, operational visibility and control. Understanding where vulnerabilities lie within production ecosystems—and how they propagate—has become a strategic imperative for both policymakers and industrial actors looking to build truly resilient industrial systems.

Energy, Competitiveness, and the European Dilemma

Europe—and Italy in particular—faces a structural challenge that goes beyond energy policy alone. Energy dependency Europe has become a core competitiveness issue, directly affecting industrial costs, investment decisions, and the resilience of strategic value chains.

Following the rapid reduction in reliance on Russian gas, Europe has not exited the risk landscape. New geopolitical tensions are once again exerting upward pressure on energy prices, increasing the likelihood of inflationary stress—and, in certain scenarios, even stagflation—at a time when industrial margins are already under pressure. In this context, energy security Italy relies on, affordability, and industrial policy have become deeply intertwined.

As a result, the strategic debate around European energy policy and the ideal energy mix is evolving. There is growing convergence around several key points:

- Renewable energy alone is not sufficient to guarantee system stability, price predictability, and industrial continuity, particularly for energy-intensive sectors.

- Nuclear energy Europe is returning to the policy agenda, not as a substitute for renewables, but as a complementary source of firm, low-carbon power. In particular, Small Modular Reactors (SMRs Europe) are increasingly framed as an industrial and energy-security opportunity at European level.

- Hybrid energy systems, combining renewables, nuclear, and storage, are emerging as the most viable pathway to reconcile industrial decarbonization objectives with competitiveness and energy supply security.

For Italy, this European energy transition is not only about strategic energy autonomy. It is also about industrial positioning within Europe’s next-generation energy and manufacturing landscape. Re-entering the nuclear value chain, particularly in advanced and modular technologies, could generate several strategic effects:

- Strengthening domestic technological capabilities, leveraging Italy’s existing expertise in engineering, manufacturing, and complex systems.

- Reducing industrial energy resilience and structural dependency risks by diversifying the sources of stable, dispatchable energy that support renewables and storage, rather than relying exclusively on imported technologies or materials.

- Supporting energy-intensive industries that underpin a significant share of Italian exports—such as manufacturing, chemicals, and advanced materials—by improving cost predictability and operational continuity.

In this emerging framework, energy choices increasingly shape industrial outcomes. The question of energy security and industrial competitiveness is no longer how to generate power, but how to align energy systems with long-term competitiveness, strategic autonomy, and the governance of complex supply chains.

The Missing Layer: Traceability as Industrial Infrastructure

Across all these dimensions—investment, industrial policy, geopolitics, and energy, a common requirement clearly emerges: absolute value chain visibility.

As supply chains become more exposed to geopolitical shocks, regulatory pressure intensifies, and capital allocation becomes more risk-sensitive, both companies and governments face the same underlying constraint: the lack of reliable, structured, and shared information across complex value chains.

To attract investment, manage supply chain exposure, mitigate operational risk, and prepare for incoming regulation, market actors increasingly need:

- Supply chain transparency and Transparent data across value chains, covering origin, composition, and transformation stages

- Advanced supply chain visibility and Real-time or near-real-time monitoring of materials, components, and critical flows

- Verified, interoperable information systems and industrial data systems that can be shared across organizational and national boundaries

This is the point at which traceability stops being a functional add-on and becomes critical industrial infrastructure.

That shift is already reflected in corporate investment priorities. According to recent industry data, 74% of companies plan to increase investment in supply chain technologies to improve operational performance, strengthen resource allocation, and generate more measurable business outcomes.

What matters, however, is not only the scale of investment, but the logic behind it. Companies are no longer investing in isolated digital tools. They are building the capabilities required to make supply chains more visible, responsive, and governable under conditions of rising volatility.

This includes investment in areas such as:

- Automated data collection and structuring, to reduce fragmentation and improve data usability

- Demand forecasting and planning, to anticipate disruptions and align supply with changing market conditions

- AI-enabled tools, to support faster and more informed decision-making

- Logistics and transport efficiency, to reduce delays, costs, and operational bottlenecks

- Process redesign and optimization, to improve resilience and performance across production systems

- Production planning and control, to strengthen execution in unstable environments

- Smart data visualization, to turn complex operational information into actionable insight

- Supply chain optimization, to improve coordination across suppliers, sites, and flows

- Sustainability and circular economy capabilities, to align industrial operations with regulatory and market expectations

- Vendor rating and supply risk management, to detect vulnerabilities before they become disruptions

Taken together, these are not isolated efficiency initiatives. They are the operational foundations of a more traceable, resilient, and strategically manageable industrial system.

In this sense, traceability is not a narrow compliance tool, but a strategic enabler that serves distinct—yet interconnected—needs:

- For investors, it reduces information asymmetry, strengthens due diligence on supply chain risk, and improves confidence in long-term value creation by making dependencies and exposures more visible.

- For policymakers, it supports the mapping of strategic dependencies, enables more evidence-based industrial policy, and allows intervention at sector and material level rather than through blunt, economy-wide measures.

- For companies, it strengthens operational control, improves resilience to disruptions, and enables faster response to shocks by making vulnerabilities identifiable before they translate into production losses or margin pressure.

Within the European context, this shift is being formalized through traceability regulation. Under the Ecodesign for Sustainable Products Regulation (ESPR), the European Union is introducing the Digital Product Passport (DPP) as a mandatory digital data framework for a growing number of product categories. The DPP is designed as a digital container of product-specific information, machine-readable product data, linked to the physical product via a data carrier, that enables traceability and transparency across the full lifecycle.

The scope of this initiative is deliberately systemic. To satisfy EU Digital Product Passport requirements, starting with batteries and expanding to textiles, electronics, metals, and other industrial goods, Digital Product Passports will require companies to provide standardized, machine-readable, and verifiable data on materials, origin, sustainability characteristics, and compliance status. Products without a compliant DPP will progressively lose access to the EU market.

In this context, traceability is no longer an optional capability or the best practice adopted by front runners. It is becoming a traceability compliance Europe systemic requirement, embedded in how the European industrial system governs risk, allocates capital, and enforces policy across borders and value chains.

From Attractiveness to Accountability

Italy strategic autonomy and industrial policy initiatives reflect a convergence of structural factors:

- A clearer long-term industrial vision, anchored in initiatives such as Made in Italy 2030

- A stronger role in global value chains, backed by manufacturing depth and specialized traceability technology capabilities

- A volatile geopolitical backdrop that has increased the premium on traceable supply chains and resilient, export-oriented industrial systems

Together, these forces position Italy as a credible destination for capital in a fragmented, uncertain environment.

But attractiveness alone is not a strategy. Sustaining momentum requires a shift in how the industrial system is governed.

What is changing is not only the scale of ambition, but the logic of industrial governance: from attracting capital to managing complexity, and from industrial policy to industrial intelligence.

Competitiveness will depend less on incentives and more on the ability to map and govern interconnected risks across supply chains, energy systems, and industrial ecosystems.

That is where data-driven supply chain traceability becomes decisive.

Not as a compliance addition, but as the link between investment, policy, and operations. It enables comprehensive ESG traceability and accountability without reducing flexibility, helping actors move from reactive decisions to anticipatory control.

In a period of geopolitical uncertainty, expanding regulation, and technological interdependence, countries and companies that make value chains visible, verifiable, and intelligible will be better able not only to attract capital, but to retain it, deploy it effectively, and translate it into sustainable industrial value.